Navigating the complexities of the U.S. tax code in 2026 requires a strategic approach, especially as the real estate market continues to evolve under the influence of the One Big Beautiful Bill Act (OBBBA) and the 21st Century ROAD to Housing Act. For homeowners and investors alike, the goal remains the same: maximizing the return on a property sale by legally minimizing the bite taken by capital gains taxes. The 2026 framework for tax optimization is built on three primary pillars: the Section 121 exclusion for primary residences, the strategic use of 1031 exchanges for investment properties, and a meticulous understanding of the updated 2026 tax brackets and deductions.

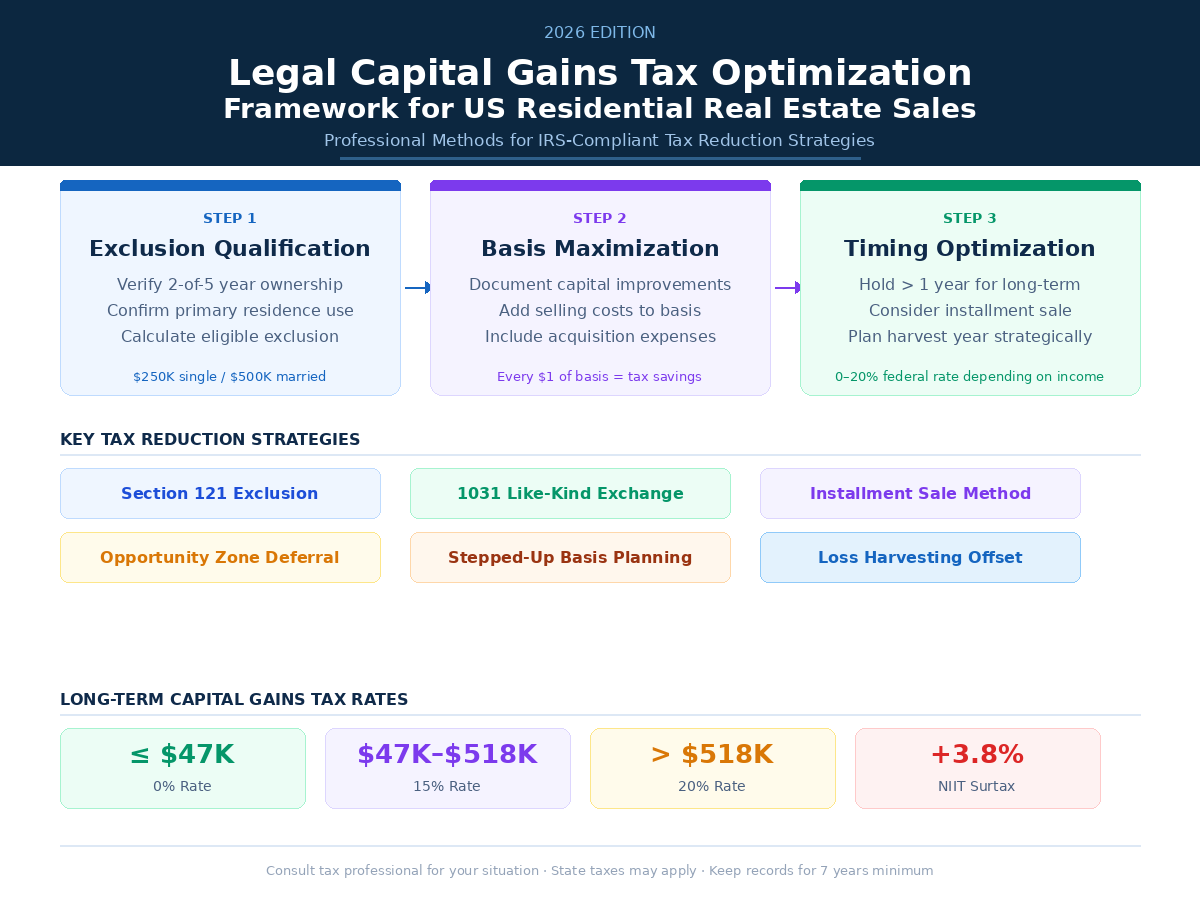

For most Americans selling their primary home, the Section 121 exclusion remains the most powerful tool in the shed. As of May 2026, the IRS continues to allow single filers to exclude up to $250,000 of capital gains from their taxable income, while married couples filing jointly can exclude up to $500,000. To qualify for this significant tax break, you must meet the “two-out-of-five-year” rule, meaning you owned and lived in the home as your principal residence for at least 24 months during the five years leading up to the sale. A common optimization strategy in 2026 involves timing the sale to ensure these windows are met, or leveraging “partial exclusions” if a move is forced by a change in employment, health issues, or other unforeseen circumstances. For instance, if you’ve only lived in your home for one year but must move for a job that is at least 50 miles further away, you may still be eligible for 50% of the exclusion.

Investors, however, face a different set of rules. While primary residences are shielded by Section 121, investment properties are subject to capital gains on the full profit unless a 1031 exchange is utilized. Despite years of legislative debate, the 1031 “like-kind” exchange remains fully intact in 2026, allowing investors to defer 100% of their capital gains and depreciation recapture taxes by reinvesting the proceeds into a new investment property. The framework for a successful exchange is rigid: you have exactly 45 days from the sale of your “relinquished” property to identify a “replacement” property and 180 days to close the deal. In the current 2026 environment, where inventory can be tight, savvy investors are identifying their replacement properties well before they even list their current holdings to avoid missing these non-negotiable IRS deadlines.

One of the most significant shifts in the 2026 tax landscape is the increased State and Local Tax (SALT) deduction cap, which was boosted to $40,000 under the OBBBA. For sellers in high-tax states like California, New York, or New Jersey, this provides a much-needed buffer, allowing for a larger deduction of property and state income taxes against their federal liability. Additionally, the 2026 long-term capital gains brackets have been adjusted for inflation. For the 2026 tax year, the 0% rate applies to single filers with taxable income up to $49,450 and married couples up to $98,900. The 15% rate covers income up to $545,500 for individuals and $613,700 for joint filers, with anything above those thresholds taxed at 20%. High-income earners must also account for the 3.8% Net Investment Income Tax (NIIT), which applies to those with a modified adjusted gross income over $200,000 (single) or $250,000 (married).

Optimization also happens at the “basis” level. Every dollar spent on capital improvements—such as a new roof, a kitchen remodel, or a finished basement—is added to your property’s cost basis, which directly reduces the taxable gain upon sale. In 2026, maintaining a digital “basis diary” with receipts and contracts is essential. While routine repairs like painting or fixing a leak do not count, permanent improvements do. By combining a maximized cost basis with the Section 121 exclusion or a 1031 exchange, and staying mindful of the 2026 income thresholds, sellers can navigate the current real estate market with a framework that prioritizes wealth preservation and long-term financial health. As always, because individual tax situations vary, consulting with a qualified tax professional is the final, critical step in any real estate exit strategy.

Leave a Reply