Introduction

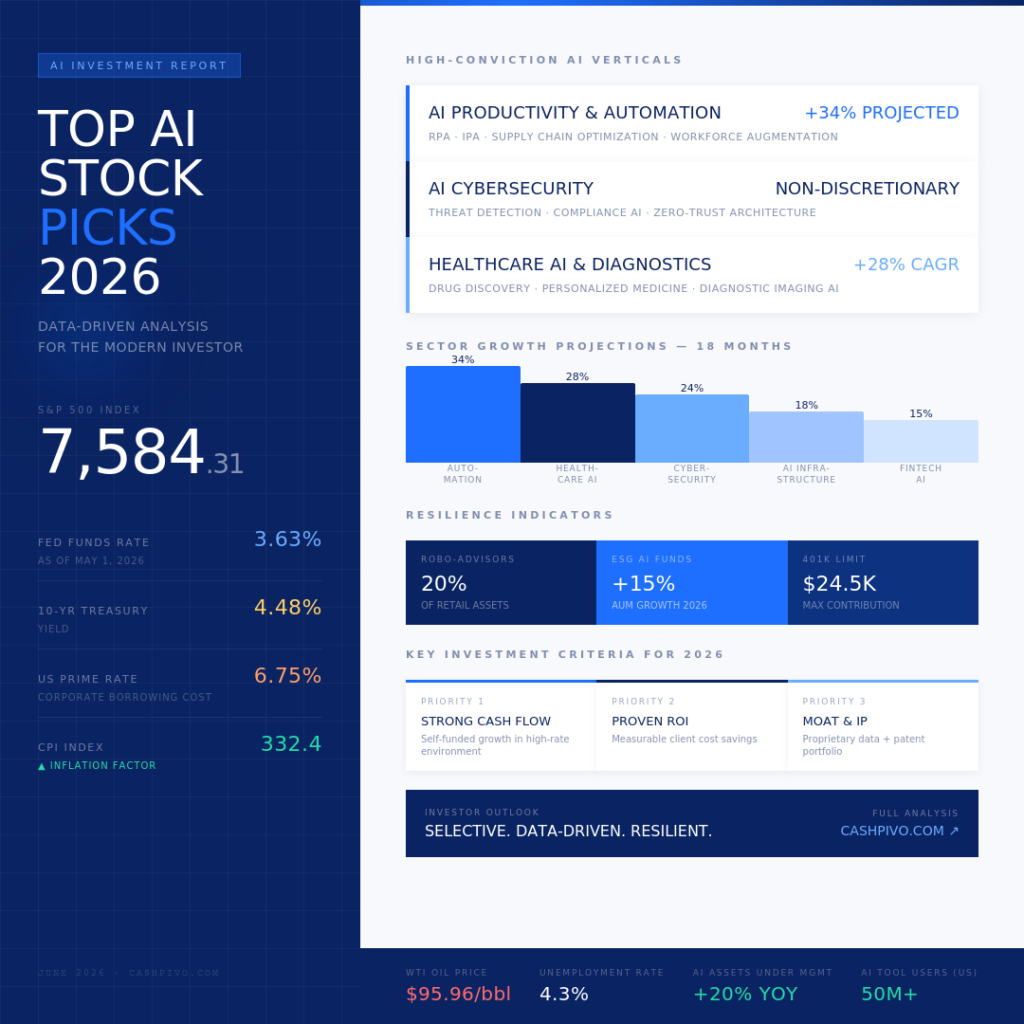

Welcome to the cutting edge of investing in 2026, where artificial intelligence isn’t just a buzzword – it’s the engine driving significant market shifts. Investors everywhere are asking: “Where are the best AI stock picks for 2026?” It’s a critical question, especially as we observe the evolving economic landscape. Just this morning, the Federal Reserve data released on June 1, 2026, painted a clear picture: the S&P 500 stands robustly at 7584.31, reflecting a market that, despite some prevailing headwinds, continues to find strength. However, the macro environment demands our attention. With the Federal Funds Rate at 3.63% as of May 1, 2026, and the 10-Year Treasury Yield at 4.48%, the cost of capital and the discount rate for future earnings are factors no investor can ignore. These figures underscore a reality where capital isn’t cheap, and valuation models need careful recalibration. This comprehensive guide will delve into the AI sector, scrutinizing areas poised for substantial growth and offering actionable insights into potential investment opportunities, keeping our current economic realities firmly in view. We’ll explore how AI’s relentless march forward intersects with today’s financial climate, offering a roadmap for astute investors.

The Macroeconomic Landscape Shaping AI Investments in 2026

To understand where AI stock picks might thrive in 2026, we first need to appreciate the economic backdrop. It’s not enough to simply bet on innovation; we must consider the environment in which these companies operate and grow. The figures we’re seeing from the Federal Reserve tell an important story. For instance, the US Prime Rate, which heavily influences corporate borrowing costs, stands at a notable 6.75%. This isn’t just an abstract number; it means that AI companies, particularly those in their high-growth phase requiring external capital for research, development, and expansion, are facing higher financing expenses. Companies with strong balance sheets and positive cash flow will be better positioned to weather this, while those heavily reliant on debt might find their growth trajectory constrained. This environment encourages a focus on profitability and sustainable business models, rather than just pure top-line growth.

Furthermore, the CPI Inflation Index, recorded at 332.407, indicates that inflationary pressures are still a significant consideration. While perhaps not as headline-grabbing as in previous years, this persistent inflation impacts everything from raw material costs for hardware manufacturers to wage demands for highly skilled AI talent. Companies with strong pricing power or those whose AI solutions offer significant cost savings for their clients are likely to outperform. AI firms that can demonstrate clear, measurable ROI for businesses seeking to optimize operations and reduce expenses in an inflationary environment will find a ready market. The broader S&P 500’s current level of 7584.31 suggests a market that has largely absorbed these realities, but selectivity is paramount. We’re looking for AI companies that aren’t just innovative but also resilient in a higher-rate, inflationary economy. This macroeconomic lens helps us narrow down the AI universe, focusing on companies with robust fundamentals that can thrive, not just survive, in 2026.

Key Growth Verticals for AI in the Current Economy

When considering AI stock picks for 2026, it’s crucial to pinpoint the specific verticals where artificial intelligence is not only making significant technological strides but also demonstrating clear economic value, especially within our current financial climate. We’re past the stage of speculative bets on unproven concepts; today, investors demand tangible returns. One of the most promising areas is AI-driven productivity and automation solutions. With the Unemployment Rate holding steady at 4.3%, according to the Federal Reserve data, businesses are still grappling with a tight labor market and the need to maximize output from their existing workforce. AI tools that automate repetitive tasks, optimize supply chains, or enhance operational efficiency are in high demand. Think about sectors like manufacturing, logistics, and even white-collar process automation. Companies providing AI-powered robotic process automation (RPA), intelligent process automation (IPA), or advanced predictive analytics for inventory management will likely see robust adoption. These solutions directly address corporate needs to reduce costs and improve margins, which is particularly attractive given the current 10-Year Treasury Yield of 4.48% — making efficient capital deployment critical.

Another vertical showing immense potential is specialized AI for data security and compliance. As businesses increasingly rely on AI and digital infrastructure, the threat landscape for cyberattacks grows exponentially. The sheer volume of data and the sophistication of threats require AI to monitor, detect, and respond effectively. In an environment where every dollar spent on IT must deliver demonstrable value, AI-powered cybersecurity platforms offer superior protection and often reduce the need for extensive human oversight. Furthermore, AI in healthcare diagnostics and personalized medicine continues its rapid ascent. While regulatory hurdles can be significant, the long-term cost-saving potential and improved patient outcomes make it an attractive sector. Consider AI applications that accelerate drug discovery, improve diagnostic accuracy, or personalize treatment plans. These sectors are less susceptible to short-term market fluctuations and offer solutions to enduring, high-value problems, making them compelling AI investment targets for 2026. The shift towards practical, revenue-generating AI applications, rather than purely conceptual ones, is a hallmark of this investment era.

Identifying Resilient AI Companies for Your 2026 Portfolio

In the current economic environment, marked by a Federal Funds Rate of 3.63% (as of 2026-05-01) and ongoing inflationary pressures reflected by the CPI Inflation Index at 332.407, identifying resilient AI companies is paramount for any investor constructing their 2026 portfolio. Resilience in this context means several things: strong balance sheets, clear pathways to profitability, diversified revenue streams, and a focus on mission-critical applications rather than discretionary ones. We’re looking beyond the “hype cycle” to companies delivering tangible value. One key characteristic is their ability to leverage AI to solve pressing enterprise problems, leading to non-discretionary spending by their clients. Think about AI solutions in cloud infrastructure, enterprise software, or industrial automation. These are areas where businesses simply cannot afford to cut corners, even when budgets are tighter.

Consider companies that specialize in AI infrastructure and foundational models. These “picks and shovels” providers, offering the computational power, specialized chips, and core AI models that underpin countless applications, are often more insulated from specific market fluctuations. As more companies adopt AI, the demand for these foundational layers only grows. Another indicator of resilience is a company’s ability to demonstrate clear return on investment (ROI) for its clients, particularly in cost-saving measures. With WTI Oil Price at $95.96/barrel, for example, companies that leverage AI to optimize logistics and reduce fuel consumption are directly addressing a critical cost center for many businesses, making their solutions highly attractive. Similarly, AI firms that enhance customer experience and retention, thereby boosting revenue and loyalty, are offering indispensable value. Finally, look for companies with strong intellectual property and a clear competitive moat. In a rapidly evolving field like AI, proprietary algorithms, extensive datasets, and robust patent portfolios can provide a significant advantage, ensuring long-term staying power. Focusing on these attributes allows investors to move beyond fleeting trends and identify AI companies truly built to last and generate value in 2026 and beyond.

Frequently Asked Questions About AI Stock Picks in 2026

Q1: How do current interest rates impact AI stock valuations in 2026?

A1: Current interest rates significantly impact AI stock valuations. With the Federal Funds Rate at 3.63% as of May 1, 2026, and the US Prime Rate at 6.75%, the cost of borrowing for companies is higher. This particularly affects high-growth AI companies that might rely on debt to fund expansion or research. Higher rates also mean that future earnings are discounted at a higher rate in valuation models, making highly speculative or non-profitable AI ventures less attractive compared to those with strong cash flow and proven profitability. Investors tend to favor companies that can self-fund growth or generate profits sooner in a higher-rate environment.

Q2: What role does inflation play when considering AI investments this year?

A2: Inflation, as indicated by the CPI Inflation Index at 332.407, is a crucial factor. Persistent inflation can lead to higher operational costs for AI companies, including increased wages for skilled talent, higher energy costs (especially relevant with WTI Oil Price at $95.96/barrel for data centers), and rising hardware component prices. This can erode profit margins. Investors should seek AI companies whose solutions help their clients combat inflation (e.g., through cost savings, efficiency gains, or supply chain optimization) or those that possess strong pricing power themselves, allowing them to pass on increased costs without losing market share.

Q3: Are there specific sub-sectors within AI that are more resilient to economic downturns in 2026?

A3: Yes, certain AI sub-sectors tend to be more resilient, particularly those offering mission-critical solutions that save money or enhance security. AI in cybersecurity, for example, is non-discretionary for most businesses. AI-driven automation and efficiency tools that directly reduce labor costs or optimize supply chains are also highly resilient, as businesses prioritize cost savings in challenging economic times. The core infrastructure providers for AI, such as specialized chip manufacturers or cloud providers, also show resilience as the foundational demand for AI continues to grow regardless of specific application success.

Q4: How does the S&P 500 performance influence AI stock selection for 2026?

A4: The S&P 500’s current level of 7584.31 provides a general barometer of market sentiment and overall economic health. A strong S&P 500 suggests a healthy market with investor confidence, which can be beneficial for AI stocks, especially those in the growth category. However, in a market at this level, investors are often more discerning. While the overall market may be strong, individual AI companies are still scrutinized for fundamentals, profitability, and sustainable growth drivers. It implies that while opportunities exist, a “rising tide lifts all boats” mentality isn’t sufficient; selective, data-driven investing is key.

Q5: What due diligence should I conduct before investing in an AI stock in 2026?

A5: Thorough due diligence is more critical than ever. Beyond checking financial health and profitability, analyze the company’s competitive moat: what proprietary technology, data, or partnerships do they possess? Evaluate their management team’s experience and vision. Understand their target market and how their AI solutions solve real-world problems. Assess their customer acquisition and retention strategies, particularly if they are enterprise-focused. Finally, consider their valuation in light of the current interest rate environment (e.g., 10-Year Treasury Yield at 4.48%), ensuring that their growth prospects justify their current price and that they aren’t overleveraged in a high-interest rate climate. Look for companies with clear paths to generating free cash flow.

Conclusion

The landscape for AI stock picks in 2026 is one of immense opportunity, yet it’s also shaped by distinct economic realities that demand a discerning eye. We’ve seen that while the S&P 500 holds strong at 7584.31, indicating a resilient broader market, the prevailing financial currents – including a Federal Funds Rate of 3.63% and an elevated CPI Inflation Index of 332.407 – necessitate a strategic approach to AI investing. The days of simply chasing speculative growth are evolving into a demand for proven value, profitability, and operational resilience.

Our exploration has highlighted that the most compelling AI investment opportunities will likely be found in companies providing mission-critical solutions: those driving productivity and automation, bolstering cybersecurity, or delivering transformative benefits in sectors like healthcare, where the ROI is clear and undeniable. We’re looking for the “picks and shovels” providers of the AI revolution, alongside those directly helping businesses navigate the challenges of a higher-cost, higher-interest-rate environment.

The message is clear: AI is not merely a technological wave; it’s an economic imperative. For investors seeking to capitalize on this transformative trend, the key isn’t just identifying AI companies, but identifying resilient AI companies that can thrive amidst today’s economic realities. Do your homework, focus on fundamentals, and look for businesses that are not just innovative but also inherently valuable and financially robust.

Ready to strategically position your portfolio for the future of AI? Dive deeper into specific companies within these high-growth verticals and consider how their business models align with the economic realities of 2026. Consult with a financial advisor to tailor your AI investment strategy to your personal financial goals and risk tolerance. The future of AI investing is here, and with careful analysis, it promises significant rewards.