As of May 21, 2026, the American financial landscape has reached a critical inflection point, demanding a more sophisticated approach to passive investing than the “set it and forget it” mantras of the previous decade. While the S&P 500 continues to show resilience, fueled by a massive $700 billion surge in artificial intelligence capital expenditures from the “Magnificent Seven,” the broader economic environment is shifting. With the Federal Reserve recently signaling a hawkish tilt in its May minutes—holding rates at 3.5% to 3.75% while warning of potential hikes to combat 3.8% inflation—investors must look beyond simple domestic large-cap exposure. Decadal wealth optimization in 2026 requires a professional framework that integrates the latest legislative shifts, specifically the permanent tax structures established by the One Big Beautiful Bill Act (OBBBA) and the evolving contribution limits for retirement vehicles.

1. Maximizing Regulatory Thresholds and Tax Diversification

The cornerstone of a 2026 strategy begins with maximizing the newly adjusted IRS contribution limits. For the current tax year, the individual 401(k) elective deferral limit has climbed to $24,500, while the IRA limit has reached $7,500. For professionals over 50, the catch-up provision now stands at $8,000.

A critical regulatory shift from the SECURE 2.0 Act has finally taken full effect: if your 2025 earnings exceeded $150,000, these catch-up contributions must now be directed into Roth accounts. This “forced” tax diversification is a boon for decadal planning, as it builds a tax-free bucket of capital that hedges against potential future rate increases. By fully utilizing these higher thresholds, an investor can shield a significantly larger portion of their wealth from the 37% top marginal rate, which the OBBBA made permanent for those earning over $640,600.

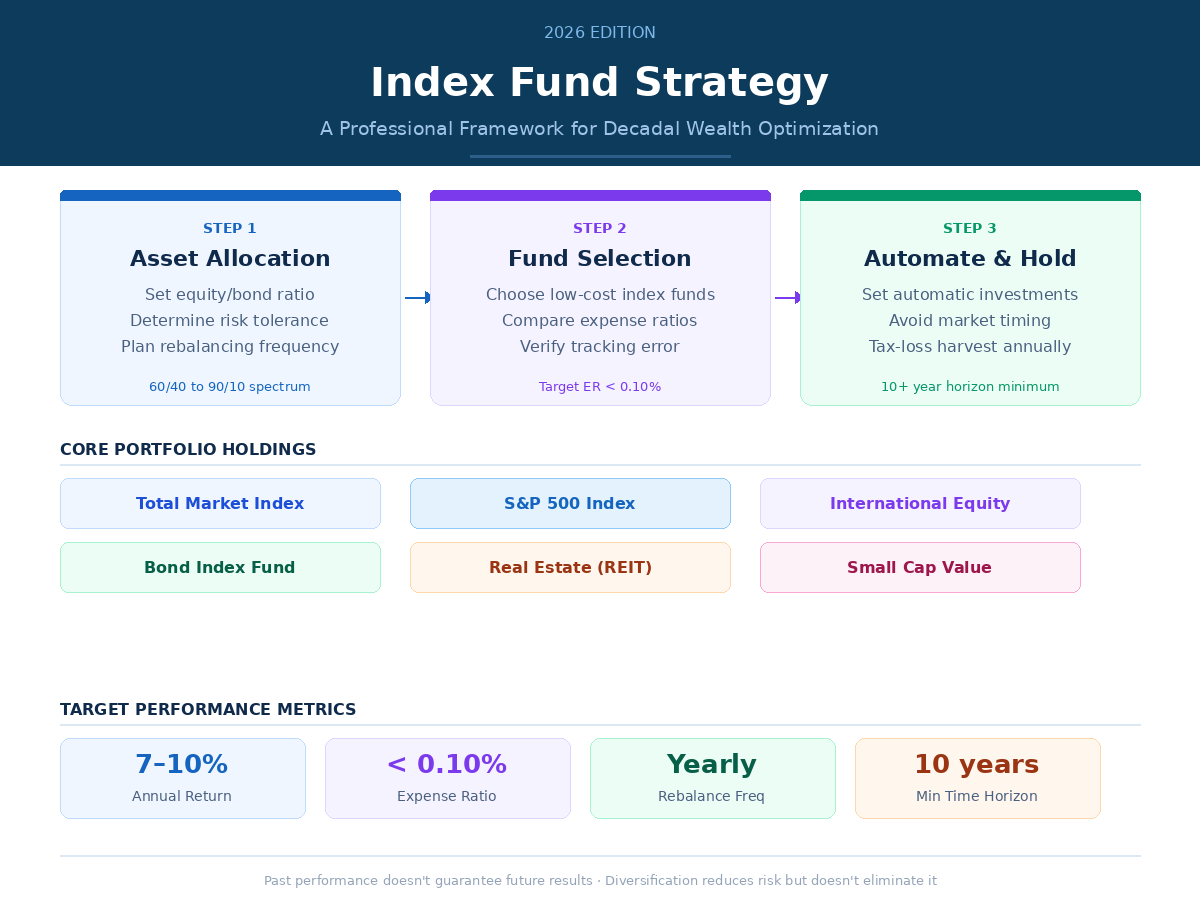

2. The “Barbell” Approach to Index Allocation

While the AI-driven “melt-up” has pushed the S&P 500 toward a year-end target of 7,600, professional frameworks are increasingly adopting a “barbell” approach to index fund allocation:

- Growth Core: Maintain exposure to technology-heavy growth indexes to capture the 40% of earnings growth currently driven by AI integration.

- Strategic Rotation: Strategically rotate into undervalued sectors like energy and small-cap stocks. The S&P SmallCap 600 is currently projected to outperform large-caps over the next five years, provided the Fed navigates the “oil crunch” without a hard landing. Diversifying into a total market index or a dedicated small-cap fund like VIOO allows investors to capture the recovery of smaller firms disproportionately suppressed by the “higher-for-longer” interest rate environment.

3. Tax Efficiency via Modern Tools

Tax efficiency has evolved with the rise of direct indexing and the OBBBA’s revision of the SALT (State and Local Tax) deduction cap. For those in high-tax states, the SALT cap has been raised to $40,000 for households earning under $500,000, providing a significant reprieve.

Sophisticated investors are moving away from traditional mutual funds in favor of ETFs and direct indexing strategies that allow for granular tax-loss harvesting. In 2026’s volatile market, marked by geopolitical tensions, harvesting losses in underperforming sectors while maintaining overall market beta can offset capital gains from high-performing tech sectors, effectively boosting net-of-tax returns by 1% to 2% annually.

4. The Global Growth Hedge

Finally, a professional framework for the late 2020s must account for global diversification. With the MSCI Emerging Markets index currently trading at a significant valuation discount compared to the U.S. market, the next decade of wealth optimization involves a heavier international tilt than the 2010s. As the U.S. economy grapples with energy price volatility, emerging markets offer a necessary growth hedge.

Conclusion

The 2026 strategy is not about abandoning the S&P 500; it is about recognizing that the “easy money” era has concluded. By combining aggressive retirement account utilization, a barbell allocation between growth and undervalued sectors, and granular tax-loss harvesting, investors can build a resilient portfolio capable of weathering the decade’s unique macroeconomic challenges.

Leave a Reply