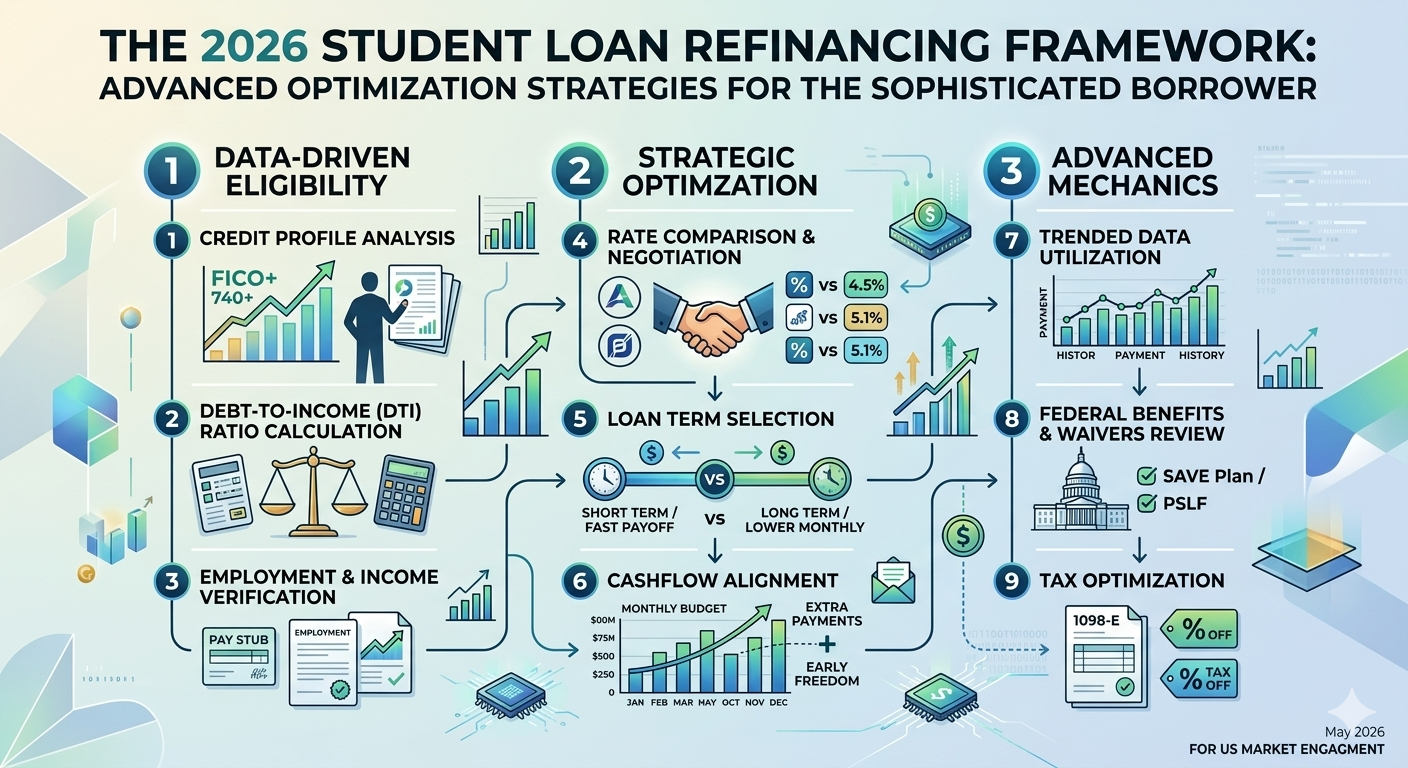

As of May 21, 2026, the American student loan landscape has reached a critical inflection point, demanding a level of strategic rigor previously reserved for corporate debt restructuring. With the full implementation of the One Big Beautiful Bill Act (OBBBA) looming on July 1st, sophisticated borrowers are navigating a market defined by the sunsetting of the SAVE plan and the emergence of the Repayment Assistance Plan (RAP). This transition, coupled with a Federal Reserve that has maintained a “higher-for-longer” stance at 3.5–3.75% despite the inflationary pressures of the ongoing conflict in the Middle East, has created a unique arbitrage opportunity for those with high-tier credit profiles. The sophisticated borrower no longer views student debt as a static obligation but as a dynamic component of a broader capital allocation strategy.

The current macro-environment presents a stark divergence between federal and private interest rates. While federal undergraduate rates for the 2025-2026 cycle sat at 6.39% and Graduate Direct Unsubsidized loans reached 7.94%, the private refinancing market has become aggressively competitive. Top-tier borrowers are currently seeing fixed-rate offers as low as 3.65%, creating an interest rate delta of over 400 basis points for graduate professionals. In a world where core PCE inflation has re-accelerated to 4.3% due to AI-driven hardware costs and energy volatility, locking in a private rate below the rate of inflation represents a significant “real” reduction in debt burden. However, the decision to refinance is no longer a simple mathematical exercise; it is a risk-adjusted trade-off against the thinning federal safety net.

Under the OBBBA, the federal government is phasing out the Grad PLUS program and imposing strict lifetime borrowing caps, which has fundamentally altered the value of federal protections. For many, the new RAP plan—which replaces the more generous SAVE plan—offers a streamlined but potentially more expensive path to forgiveness. Sophisticated borrowers must now weigh the “insurance premium” of federal protections against the immediate liquidity gains of private refinancing. If your debt-to-income ratio is low and your career trajectory is stable, the 4% interest savings found in the private market often outweigh the value of a federal “safety net” that has become increasingly restrictive. This is particularly true for those in high-growth sectors like AI development or specialized medicine, where the probability of needing income-driven relief is statistically negligible.

A key pillar of the 2026 framework is the “Grandfathering Hedge.” Borrowers who held federal loans prior to the July 1, 2026, deadline have a three-year window to continue borrowing under the old, higher limits or remain on legacy repayment plans. This creates a strategic “wait-and-see” period. The sophisticated approach involves maintaining federal status for the highest-interest tranches—such as Parent PLUS loans at 8.94%—while selectively refinancing lower-balance, high-rate graduate loans into the private market. By “laddering” your debt in this manner, you preserve the ability to access federal discharge programs for a portion of your portfolio while simultaneously reducing the weighted average cost of capital across your entire balance sheet.

Furthermore, the 2026 borrower must consider the tax implications of employer-sponsored debt repayment. With Section 127 of the Internal Revenue Code now a permanent fixture of the corporate landscape, many sophisticated professionals are leveraging employer contributions as a “forced” principal reduction tool. When refinancing, it is essential to ensure that your private lender is integrated with your employer’s benefits platform. This allows for seamless, tax-free payments of up to $5,250 annually, which, when applied to a refinanced loan at 3.7%, accelerates the amortization schedule far more effectively than it would on a 7.9% federal loan.

Optimization in 2026 also requires a sophisticated view of liquidity. With the U.S. economy bolstered by an AI-driven investment boom, the opportunity cost of over-paying student debt is at an all-time high. By refinancing to a lower monthly payment, borrowers can redirect the surplus cash flow into high-yield environments or tax-advantaged investment vehicles. In this framework, student loan refinancing is not just about “getting out of debt”; it is about maximizing your net worth by ensuring your cheapest capital is working the hardest.

As we move toward the third quarter of 2026, the window for sub-4% private rates may begin to close if the Fed pivots toward a rate hike to combat sticky inflation. The sophisticated borrower should act before the July 1st regulatory shift complicates the underwriting process. By auditing your current portfolio against the 3.65% private