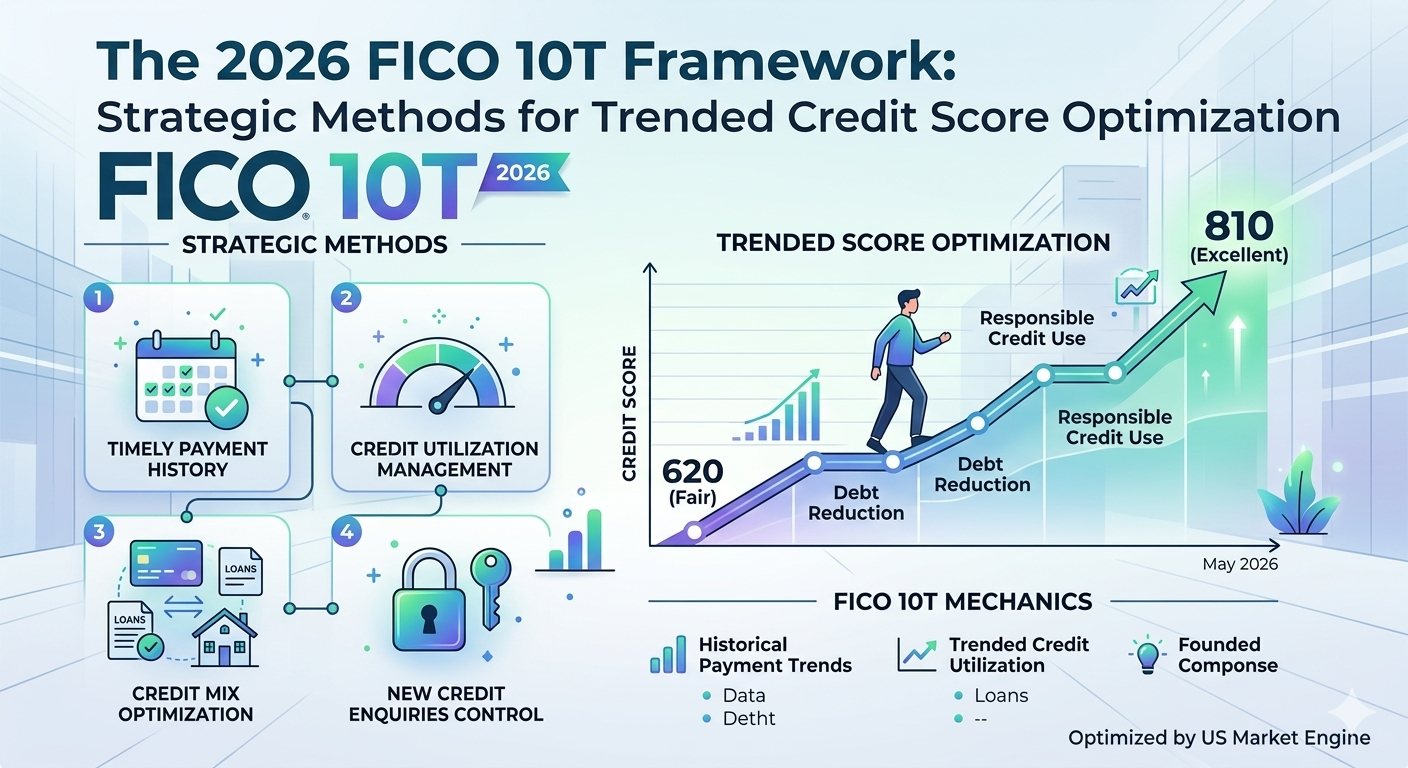

The landscape of American consumer credit is undergoing its most significant transformation in decades. As of May 21, 2026, the shift from the traditional “snapshot” credit scoring model to the FICO 10T framework has moved from a theoretical update to an operational reality for millions of borrowers. For years, the industry relied on Classic FICO models that captured a single moment in time—a frozen image of your debt and payment status on the day your report was pulled. Today, the Federal Housing Finance Agency (FHFA) and the Department of Housing and Urban Development (HUD) have officially integrated FICO 10T and VantageScore 4.0 into the mortgage ecosystem, fundamentally changing how creditworthiness is defined. The “T” in FICO 10T stands for “Trended,” and understanding this shift is the key to optimizing your financial profile in this new era of lending.

Unlike its predecessors, the FICO 10T framework analyzes a 24-month rolling window of your financial behavior. This means that a one-time payment to lower your utilization right before applying for a loan—a common tactic in the “Classic” era—is no longer a silver bullet. Instead, the model distinguishes between “transactors,” who pay their balances in full every month, and “revolvers,” who carry debt from month to month. In the 2026 credit environment, being a transactor is the highest form of credit optimization. The trended data allows lenders to see if your debt levels are rising, falling, or remaining stagnant over two years. A borrower with a 720 score whose debt is trending downward is now viewed much more favorably than a borrower with the same score whose debt has been steadily climbing for eighteen months.

Strategic optimization in 2026 requires a shift in focus toward long-term consistency. One of the most powerful levers in the FICO 10T model is the inclusion of alternative data, specifically rental and utility payment history. Following the regulatory updates earlier this spring, Fannie Mae and Freddie Mac have expanded their systems to reward consistent on-time rent payments, which were historically invisible to the major bureaus. If you are a renter, ensuring your landlord or property management company reports your data to the bureaus is no longer optional; it is a strategic necessity. For many “thin-file” borrowers, this data alone can provide the lift needed to qualify for competitive mortgage rates that were previously out of reach.

Furthermore, the 2026 framework has finally integrated Buy Now, Pay Later (BNPL) data into the scoring mix. As these short-term installment loans became a staple of American retail over the last few years, their absence from credit reports created a blind spot for lenders. Now, every BNPL payment is a data point in your 24-month trend. To optimize your score, you must treat these small installments with the same gravity as a mortgage or auto loan. Stacking multiple BNPL plans can now signal “credit thirst” or financial instability, potentially dragging down your trended score even if you never miss a payment.

The regulatory environment has also introduced new complexities regarding medical debt. While a 2025 CFPB initiative attempted to ban medical debt from reports entirely, recent federal court rulings in late 2025 and early 2026 have kept medical debts over $500 on the table in many jurisdictions. However, the FICO 10T model is designed to be more “forgiving” of these non-predictive dings compared to older models, focusing instead on your revolving credit trends. This is particularly relevant given that Fannie Mae recently eliminated its hard 620-score floor, moving toward a holistic risk assessment that weighs your cash reserves and debt-to-income ratio alongside your trended score.

To master the FICO 10T framework, you must manage your credit as a trajectory rather than a destination. Avoid “credit cycling”—the practice of maxing out and paying off a card multiple times a month—as the trended data may flag this as high-risk behavior. Instead, aim for a steady, low utilization rate that remains consistent over the 24-month look-back period. As we approach the full phase-out of legacy models in 2027, the borrowers who thrive will be those who understand that their financial past is now a living part of their financial present. By maintaining a downward trend in revolving debt and ensuring all “alternative” payments like utilities and rent are documented, you can position yourself at the forefront of the 2026 credit market, unlocking lower interest rates and greater borrowing power in an increasingly sophisticated financial world.

Leave a Reply