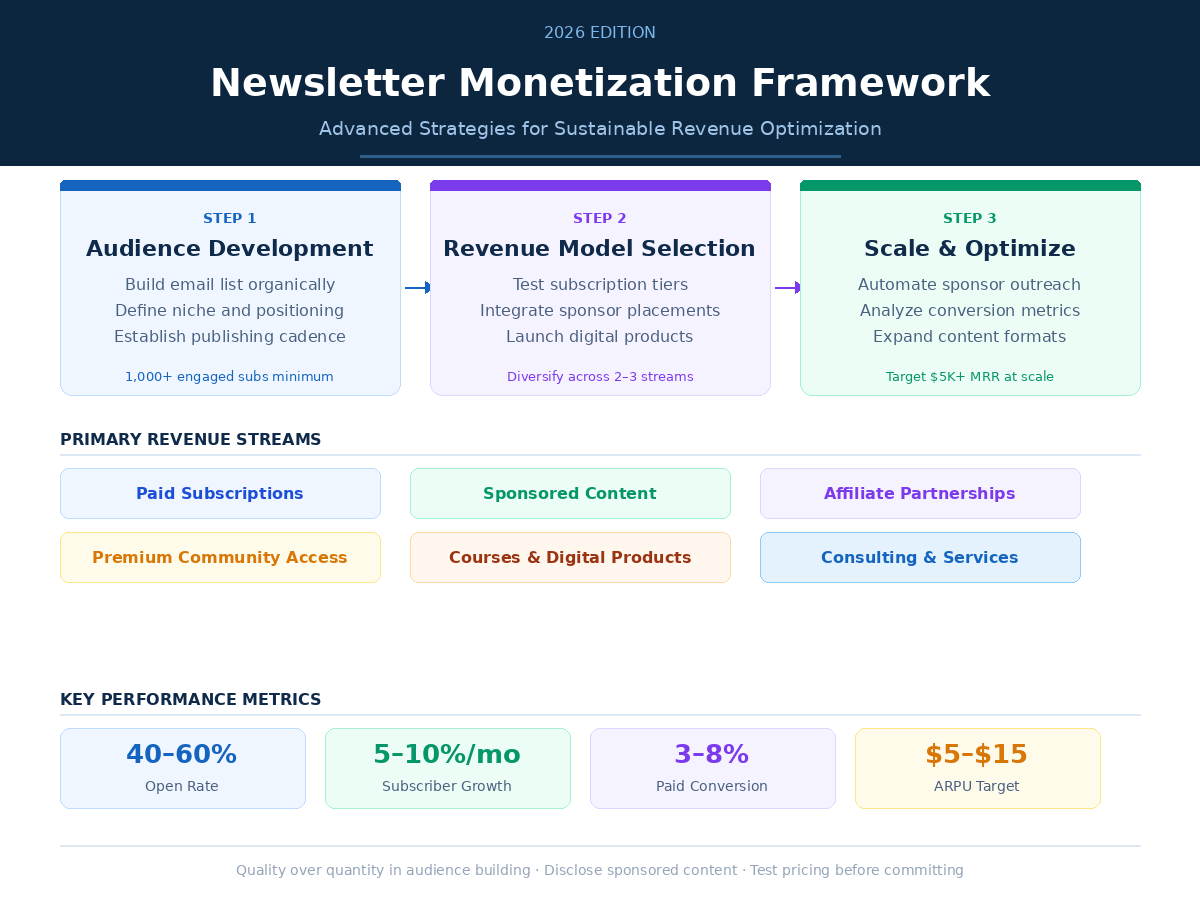

As of May 21, 2026, the landscape for newsletter monetization has shifted from a wild-west gold rush into a sophisticated, highly regulated professional ecosystem. For creators and media entrepreneurs in the United States, the “2026 Framework” for sustainable revenue is no longer just about growing an email list; it is about navigating a complex intersection of new federal tax laws, evolving consumer protection mandates, and a revitalized fintech environment. Success this year requires a dual mastery of high-value content and the administrative rigor demanded by the landmark legislation passed over the last eighteen months.

The most significant shift for the mid-tier creator comes from the One Big Beautiful Bill Act (OBBBA), which officially stabilized the digital economy in late 2025. For those who remember the years of confusion surrounding the 1099-K reporting thresholds, the current environment offers a much-needed reprieve. The permanent restoration of the $20,000 and 200-transaction threshold for third-party payment processors like Stripe and PayPal has removed a massive administrative burden for emerging newsletters. However, this does not mean record-keeping is any less vital. With the 1099-NEC and 1099-MISC thresholds now sitting at $2,000, newsletter operators must be more diligent than ever in tracking direct brand sponsorships and affiliate payouts. The OBBBA also brought a major victory for creators who develop their own proprietary tools or software-driven delivery systems: the return to 100% immediate expensing for domestic research and experimental expenditures under Section 174. This allows you to fully deduct the costs of developing custom automation or AI-driven personalization engines in the year they are incurred, providing a powerful incentive to move away from off-the-shelf platforms and toward owned infrastructure.

Monetization in 2026 also demands a “compliance-first” approach to sponsorship. The Federal Trade Commission has significantly ramped up enforcement this spring, particularly following the March 2026 Advance Notice of Proposed Rulemaking aimed at reviving the “Click-to-Cancel” rule. While the 2024 version of the rule faced a temporary setback in the courts, the FTC’s current trajectory makes it clear that “simple mechanisms” for subscription cancellation are now a non-negotiable standard for any newsletter charging a recurring fee. Furthermore, the days of relying solely on a platform’s built-in “Paid Partnership” tag are over. Current enforcement trends show that the FTC now views platform tags as insufficient on their own. To avoid fines that currently range between $51,000 and $53,000 per violation, creators must include clear, “above the fold” disclosures—such as a prominent #ad or “Sponsored by”—within the first few lines of the newsletter. This transparency is no longer just a legal hurdle; it has become a cornerstone of audience trust in an era where 78% of US consumers report that immediate disclosure increases their likelihood of engaging with a recommendation.

Beyond taxes and transparency, the 2026 framework leverages the rapid integration of fintech into traditional publishing. Just this week, the signing of the Executive Order on Integrating Financial Technology Innovation into Regulatory Frameworks has signaled a new era for how newsletters handle transactions. This order, combined with the earlier establishment of the Strategic Bitcoin Reserve in 2025, is beginning to lower the barriers for creators to accept a wider variety of digital assets and stablecoins with reduced transaction friction. For newsletter owners, this means the ability to bypass traditional banking delays and high merchant fees, particularly for international subscribers. By adopting these streamlined payment systems, creators can capture a higher percentage of their gross revenue while offering subscribers more flexible ways to pay.

Finally, sustainable revenue optimization in 2026 relies on maximizing the permanent Qualified Business Income (QBI) deduction under Section 19