In the current climate of May 2026, the United States real estate market has transitioned into a phase of disciplined stabilization. For fix-and-flip investors, the “easy wins” of the post-pandemic era have been replaced by a landscape that demands surgical precision in both project execution and financial structuring. As of today, May 21, 2026, the Federal Reserve has maintained the federal funds rate in a target range of 3.5% to 3.75%. However, with recent FOMC minutes signaling a hawkish tilt and the incoming Fed Chair Kevin Warsh set to take the helm tomorrow, private money lenders and borrowers must navigate a “higher-for-longer” reality that makes the strategic framework of a loan more critical than the capital itself.

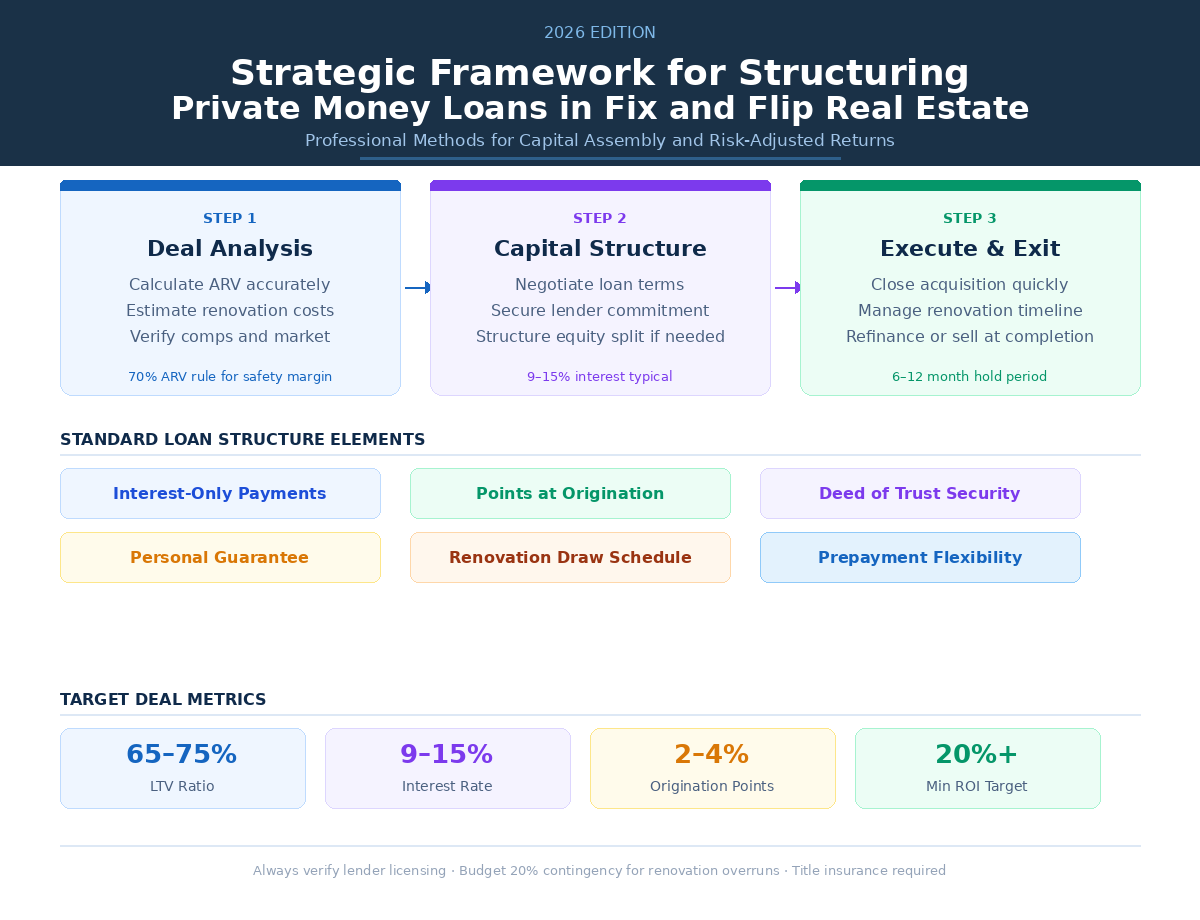

A robust framework for structuring private money loans in 2026 begins with a shift from simple asset-based lending to a more holistic, risk-adjusted underwriting model. While the median gross profit for a US flip currently hovers around $65,300, the average return on investment has compressed to approximately 25%. This margin pressure means that the traditional “70% of ARV” (After Repair Value) rule is no longer a one-size-fits-all solution. Sophisticated lenders are now utilizing a dual-cap structure, often limiting loans to 90% of total cost (LTC) while simultaneously ensuring the total leverage does not exceed 75% of the projected ARV. This protects the lender against the slight cooling of home price appreciation seen in the spring 2026 data, while providing the investor with enough leverage to keep their personal liquidity intact for unforeseen renovation hurdles.

The cost of capital in today’s market reflects this nuanced risk environment. Private money rates for seasoned flippers currently range between 8.5% and 11.5%, with origination fees typically landing between one and two points. For the borrower, the strategy lies in negotiating “interest-only” periods that align strictly with the renovation timeline. In 2026, we are seeing a rise in “staged draw” structures where interest is only charged on the disbursed funds rather than the total committed loan amount. This “Dutch interest” model is a powerful tool for investors to preserve cash flow during the early, capital-intensive phases of a project, such as foundation work or major system overhauls.

Equally critical to the 2026 framework is the evolving regulatory and tax environment. Private lenders must now account for the new IRS reporting requirements that took effect this tax season, which mandate more rigorous transparency for privately held mortgage notes, similar to the institutional Form 1098. Furthermore, the Homebuyers Privacy Protection Act, which became effective in March 2026, has fundamentally changed how “trigger leads” are handled, making it essential for lenders to maintain direct, consent-based relationships with their borrowers. In states like California, Nevada, and Utah, the push for stricter business-purpose licensing means that the “strategic” part of the framework must include a verified compliance check to ensure the loan’s enforceability and the lender’s standing.

Beyond the initial purchase and rehab, the most successful frameworks in the current market incorporate a “Plan B” exit strategy. With the 30-year fixed mortgage rate hovering near 6.23%, the traditional exit of selling to a retail buyer is being supplemented by the “fix-to-rent” model. Over 50% of active flippers in 2026 are now structuring their private money loans as “bridge-to-perm” products. This allows the investor to flip the property into a long-term Debt Service Coverage Ratio (DSCR) loan if the retail market softens during the renovation. By embedding a pre-negotiated refinance option into the initial private money structure, investors can mitigate the risk of “stale” inventory and pivot to a cash-flowing rental strategy without the stress of a looming balloon payment.

Ultimately, structuring private money loans in 2026 is an exercise in balancing speed with sustainability. While fintech-driven hard money platforms can now close in as little as three to five days, the strategic advantage goes to those who prioritize the relationship-driven nuances of the deal. This includes clear communication on draw schedules, a deep understanding of local market inventory—particularly in high-growth corridors in the South and West—and a commitment to regulatory transparency. As we look toward the second half of 2026, the investors who thrive will be those who view their private money lender not just as a source of funds, but as a strategic partner in a complex, data-driven ecosystem.

Leave a Reply