In the rapidly evolving financial landscape of 2026, the concept of a legacy has shifted from a static inheritance to a dynamic, protected continuum. For many American families, the recent passage of the One Big Beautiful Bill Act (OBBBA) has redefined the boundaries of wealth transfer, replacing the long-feared “tax cliff” of the previous decade with a robust, permanent federal estate tax exemption of $15 million per individual. While this $30 million threshold for married couples offers unprecedented breathing room, it has also birthed a new era of complexity. Establishing a legally sound family living trust is no longer just about avoiding probate; it is about implementing a Legacy Protection Framework—a strategic, multi-layered method designed to navigate modern tax codes, privacy concerns, and the intricate rules of the SECURE Act 2.0.

The foundation of this framework begins with understanding that a living trust is a living entity, not a “set it and forget it” document. As of May 2026, the most successful estate plans are those that integrate the elevated federal exemptions with the reality of state-level nuances. While the federal government has signaled stability, several states continue to enforce their own estate or inheritance taxes with much lower thresholds. For instance, residents in states like New York must still contend with the “tax cliff,” where exceeding the state exemption by even a small margin can trigger a tax on the entire estate. A strategic Legacy Protection Framework accounts for these geographic discrepancies by utilizing formula funding clauses that automatically adjust based on the current year’s state and federal limits, ensuring that no family is blindsided by a localized tax bill.

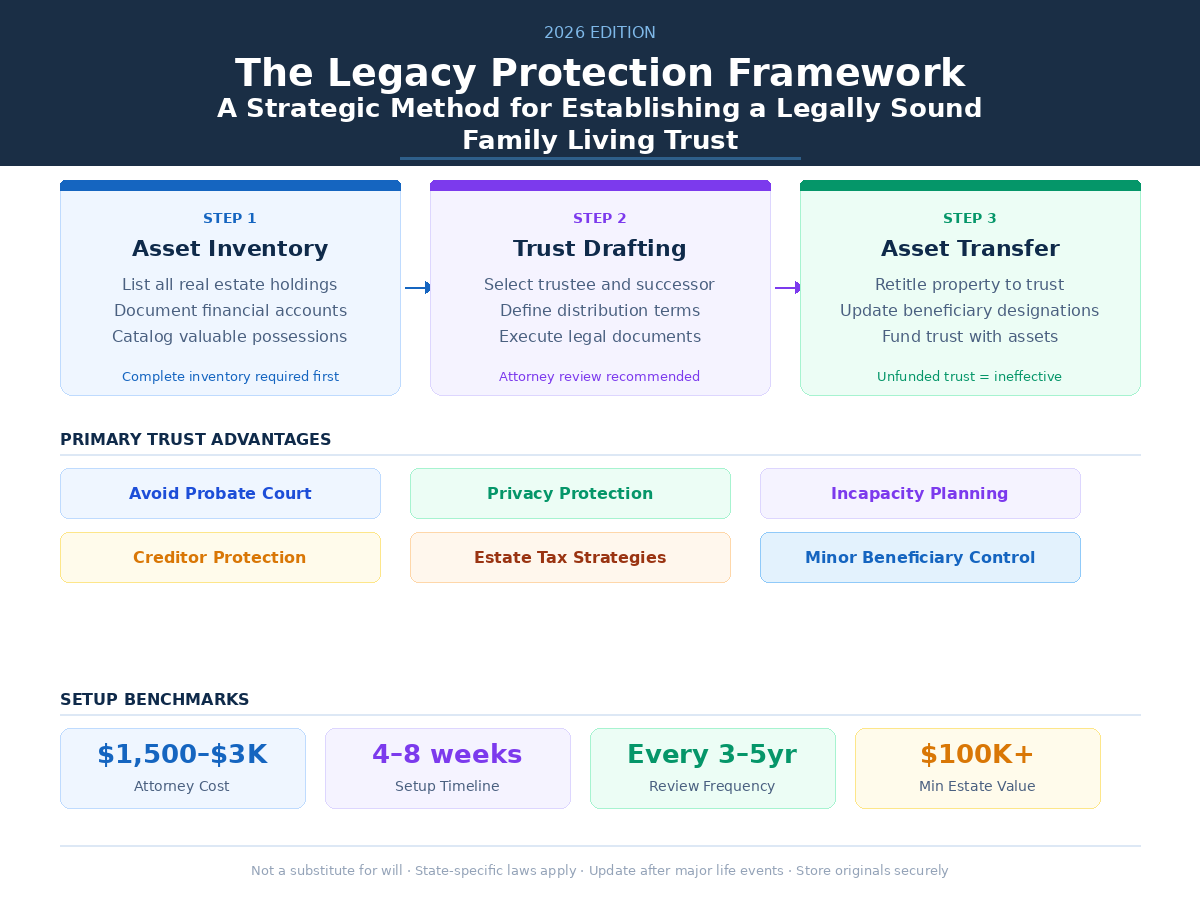

Beyond tax mitigation, the framework emphasizes the critical importance of trust funding—a step where many well-intentioned plans fail. A trust is essentially an empty vessel until it is “funded” with assets. In 2026, this process involves more than just retitling real estate or bank accounts; it requires a meticulous audit of digital assets, intellectual property, and increasingly common cryptocurrency holdings. Under the current legal standards, failure to properly transfer these assets into the name of the trust can leave them vulnerable to the very probate process the trust was designed to bypass. By systematically aligning every asset with the trust’s structure, the Legacy Protection Framework ensures that the transition of wealth is seamless, private, and immediate upon the grantor’s passing.

The integration of retirement planning into the family trust has also become a focal point this year, particularly with the SECURE Act 2.0 provisions now fully in effect. With the required minimum distribution (RMD) age having climbed to 73 for those born between 1951 and 1959, and 75 for those born in 1960 or later, the timing of wealth depletion has changed. A legally sound trust must now be drafted as a “see-through” or “conduit” trust to handle inherited IRAs properly. Without these specific legal designations, beneficiaries may be forced to withdraw the entirety of an inherited retirement account within ten years, potentially pushing them into the highest possible income tax bracket. The Legacy Protection Framework coordinates the trust’s distribution language with these RMD timelines, allowing for tax-deferred growth to continue for as long as the law allows.

Furthermore, the 2026 landscape has seen a significant rise in the use of annual gift tax exclusions as a proactive tool within the trust framework. With the current exclusion set at $19,000 per recipient—or $38,000 for married couples—families are increasingly using “Crummey” powers to fund irrevocable life insurance trusts or educational sub-trusts without tapping into their lifetime $15 million exemption. This strategy allows for the “shaving” of an estate’s value over time, moving future appreciation out of the taxable estate while providing immediate benefits to children and grandchildren. It is a proactive approach that transforms the trust from a death-benefit vehicle into a lifetime wealth-management tool.

As we look at the current trends, it is also impossible to ignore the role of technology in establishing these frameworks. While 2026 has seen a 30% increase in Americans trusting AI-driven advice for initial estate drafting, the most legally sound trusts remain those vetted by human expertise to ensure compliance with the specific fiduciary standards of each jurisdiction. A strategic method involves using modern digital tools for asset tracking and communication while relying on professional legal counsel to navigate the “gray areas” of trust law, such as decanting or the appointment of independent trust protectors.

Ultimately, the Legacy Protection Framework is about more than just numbers on a ledger; it is about the preservation of family values and the prevention of conflict. By clearly defining the roles of successor trustees and providing specific guidance on discretionary distributions, a family living trust acts as a roadmap for future generations. In an era where financial policies can shift with the stroke of a pen, the most enduring legacy is one built on a foundation of strategic foresight, rigorous legal compliance, and a commitment to protecting what matters most. For the modern American family, the window of opportunity provided by the 2026 tax environment is a call to action—a chance to secure a future that is as stable as it is prosperous.

Leave a Reply