The financial landscape of May 2026 presents a unique set of challenges for the American consumer. With the Federal Reserve, now under the leadership of Chair Kevin Warsh, maintaining the federal funds rate in the 3.5% to 3.75% range, the era of “cheap money” remains a distant memory. For those carrying credit card balances, the reality is even more stark: average APRs for new offers have climbed to approximately 23.79%, with many rewards cards pushing well past the 25% mark. In this high-interest environment, a haphazard approach to debt is no longer just inefficient; it is a significant drain on your long-term wealth. To navigate this, you need a strategic debt repayment framework that prioritizes mathematical efficiency while simultaneously shielding your credit score from the volatility of modern reporting standards.

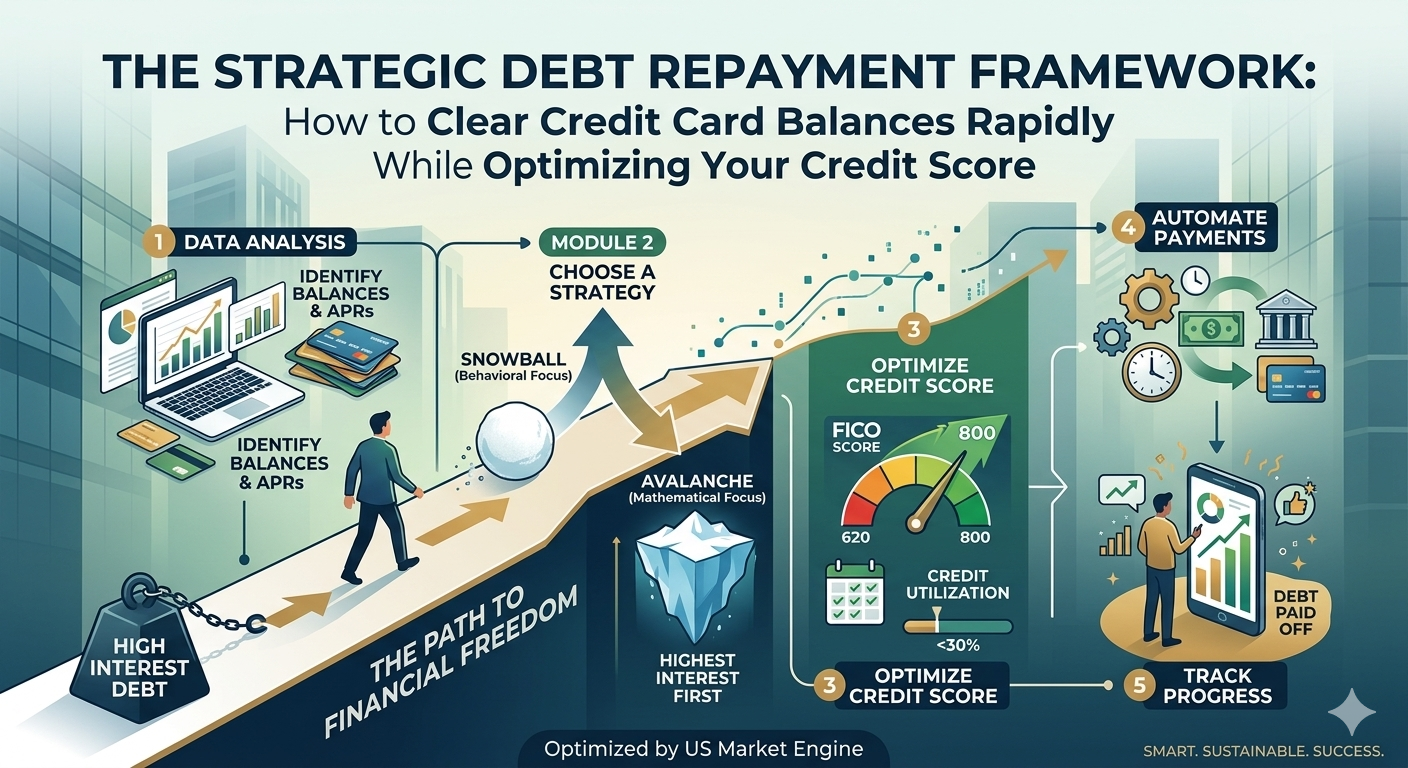

The foundation of any rapid repayment strategy in 2026 must be the “Debt Avalanche” method, which has gained renewed importance as interest rates have surged. While the “Debt Snowball” focuses on psychological wins by paying off small balances first, the Avalanche targets the highest-interest debt regardless of the balance size. In an economy where a $5,000 balance at 24% APR can accrue over $100 in interest charges every single month, the priority must be to neutralize the most expensive capital first. By making the minimum payments on all accounts and funneling every extra dollar into the card with the highest APR, you effectively “guarantee” a return on your money equal to that interest rate. This is particularly critical now that the Consumer Financial Protection Bureau’s (CFPB) attempt to cap late fees at $8 was voided by federal courts last year. With late fees still hovering between $30 and $43 for most major issuers, the cost of a single missed payment can now wipe out weeks of progress, making automated minimum payments a non-negotiable first step in your framework.

As you aggressively pay down principal, you must also manage the optics of your credit report to optimize your score. In 2026, credit scoring models like FICO 10T and VantageScore 4.0 have become more sensitive to “trended data,” meaning they look at whether your balances are rising or falling over time rather than just a single snapshot. To maximize your score, you should aim for a credit utilization ratio below 10% on each individual card, not just across your total available credit. Furthermore, be mindful of the recent integration of Buy Now, Pay Later (BNPL) plans into standard credit reports. While these installment plans were once “invisible” debt, they now factor into your debt-to-income ratio and payment history. If you are using BNPL services alongside credit cards, ensure those payments are perfectly timed, as the new reporting transparency means a single late “pay-in-four” installment can now ding your FICO score just as severely as a missed mortgage payment.

Strategic optimization also requires understanding what not to worry about. As of May 2026, the three major credit bureaus—Equifax, Experian, and TransUnion—continue their voluntary policy of excluding medical collections under $500 from credit reports, as well as any medical debt that has been paid in full. Even though the broader CFPB rule to ban all medical debt from reports was vacated in 2025, these voluntary protections remain a vital safety net. If you are balancing credit card debt alongside medical bills, prioritize the credit cards. High-interest revolving debt is a “live” threat to your score and net worth, whereas medical debt under the $500 threshold is effectively neutralized for scoring purposes. This allows you to keep your liquidity focused where it does the most work: killing off those 23%+ APR balances.

For those with credit scores still in the “Good” to “Excellent” range (700+), the 0% APR balance transfer remains the most powerful weapon in the arsenal, though the window is narrowing. Despite the Fed’s “higher for longer” stance, some issuers are still offering 12- to 15-month introductory windows to attract high-quality borrowers. However, with the Credit Card Competition Act currently moving through Congress, there is ongoing speculation that rewards programs and sign-up incentives may be scaled back if swipe fees are reduced. If you have the opportunity to lock in a 0% transfer today, do so before the market shifts. Moving a high-interest balance to a 0% card immediately halts the “interest bleed,” allowing every cent of your payment to hit the principal. Just be sure to calculate the transfer fee—usually 3% to 5%—to ensure the math still favors the move.

Ultimately, clearing credit card debt in 2026 is a game of precision. By combining the mathematical rigor of the Debt Avalanche with

Leave a Reply