As we navigate the midpoint of 2026, the American financial landscape has entered a period of profound transition that demands a recalibration of traditional income strategies. The recent leadership change at the Federal Reserve, with Kevin Warsh succeeding Jerome Powell as Chair, has signaled a definitive shift toward a more hawkish, “inflation-first” monetary policy. Coupled with the persistent energy price volatility stemming from the ongoing conflict in Iran and the expiration of the Tax Cuts and Jobs Act (TCJA) at the end of 2025, conservative investors are facing a unique “double squeeze”: higher personal tax brackets and sticky inflation that erodes the purchasing power of traditional fixed-income yields. In this environment, the 2026 Framework for Strategic Yield Optimization offers a disciplined path for generating reliable monthly income through high-yield corporate bonds without compromising the structural integrity of a conservative portfolio.

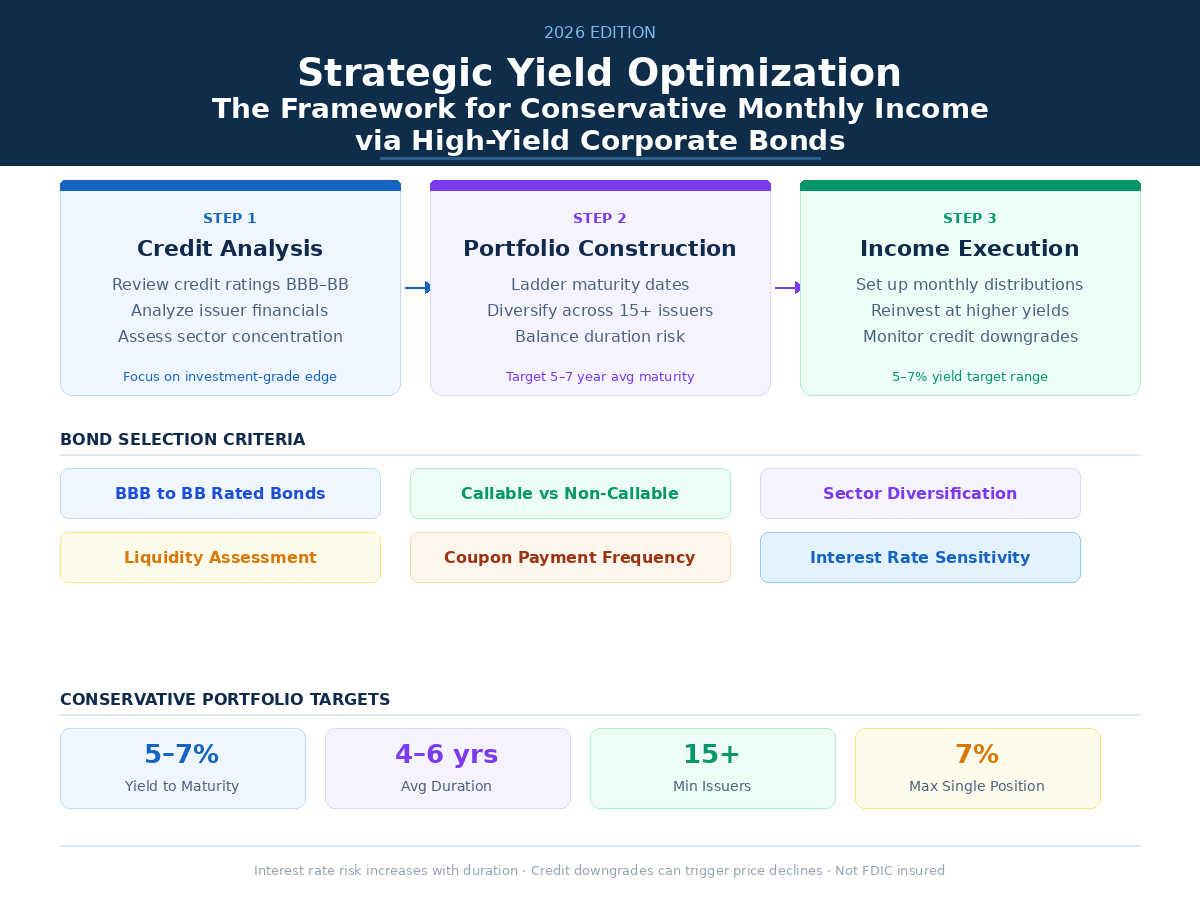

The cornerstone of this framework is a refined focus on “quality junk”—specifically, the BB-rated segment of the corporate credit market. While the term “high-yield” often conjures images of distressed debt, the 2026 market is characterized by a massive influx of “fallen angels” and AI-driven debt issuances from fundamentally sound technology and industrial firms. These companies are leveraging the current AI infrastructure boom to finance long-term growth, resulting in a robust supply of bonds that offer a significant yield premium over Treasuries. By targeting the upper tier of the high-yield spectrum, investors can capture yields currently hovering between 6.5% and 7.2%, providing a necessary buffer against a headline inflation rate that has recently accelerated to 3.8%. This “BB sweet spot” allows for a conservative posture because these issuers typically maintain stronger balance sheets and higher interest coverage ratios than their lower-rated peers, offering a layer of protection against the default risks that often plague the CCC-rated tier during periods of economic cooling.

Active duration management is the second pillar of the 2026 framework. With the Warsh-led Fed signaling that the era of rate cuts is firmly in the rearview mirror—and even hinting at potential hikes to combat energy-driven price spikes—investors must avoid the “duration trap.” Long-dated bonds are increasingly vulnerable to price depreciation as the yield curve steepens. Consequently, the current framework prioritizes a short-to-intermediate duration stance, specifically targeting maturities in the three-to-five-year range. This positioning minimizes interest rate sensitivity while allowing investors to reinvest maturing capital into the higher-coupon environments that the “higher-for-longer” regime provides. By laddering these maturities, a conservative investor can create a “yield engine” that produces consistent monthly cash flow, effectively turning market volatility into a tool for compounding rather than a threat to principal.

Tax efficiency has become an urgent priority following the sunset of the TCJA provisions on January 1, 2026. With the top individual marginal tax rate reverting to 39.6% and the standard deduction nearly halved, the “all-in” return on corporate bonds is now heavily dependent on where those assets are held. For the conservative monthly income seeker, the 2026 framework mandates the use of tax-advantaged accounts, such as Roth IRAs or 401(k)s, to shield high-coupon payments from these higher tax rates. If holding bonds in taxable accounts is unavoidable, the framework suggests a “barbell” approach: pairing high-yield corporates with the now-attractive yields found in the municipal bond market, which has seen a resurgence as state and local governments offer competitive, tax-exempt rates to fund infrastructure resilience.

Furthermore, the implementation of the Personal Financial Data Rights Rule in April 2026 has revolutionized how investors access these yields. This “open banking” mandate has made it easier than ever to move capital between institutions to find the most competitive brokerage spreads and specialized high-yield funds. Conservative investors should leverage this transparency to seek out active managers who can navigate the “K-shaped” credit market. As the AI boom continues to drive disparate outcomes across sectors, the ability to distinguish between a company issuing debt for productive innovation and one issuing debt for survival is the difference between a stable monthly check and a capital loss.

Ultimately, Strategic Yield Optimization in 2026 is not about chasing the highest possible number; it is about securing a “real” yield—one that outpaces both the IRS and the rising cost of living. By focusing on high-quality credit, maintaining a disciplined short-duration ladder, and maximizing tax-advantaged shells, US investors can build a monthly income stream that is as resilient as it is rewarding. In an era of new Fed leadership and geopolitical uncertainty, this framework provides the clarity needed to move from a defensive crouch to a position of strategic strength.

Leave a Reply