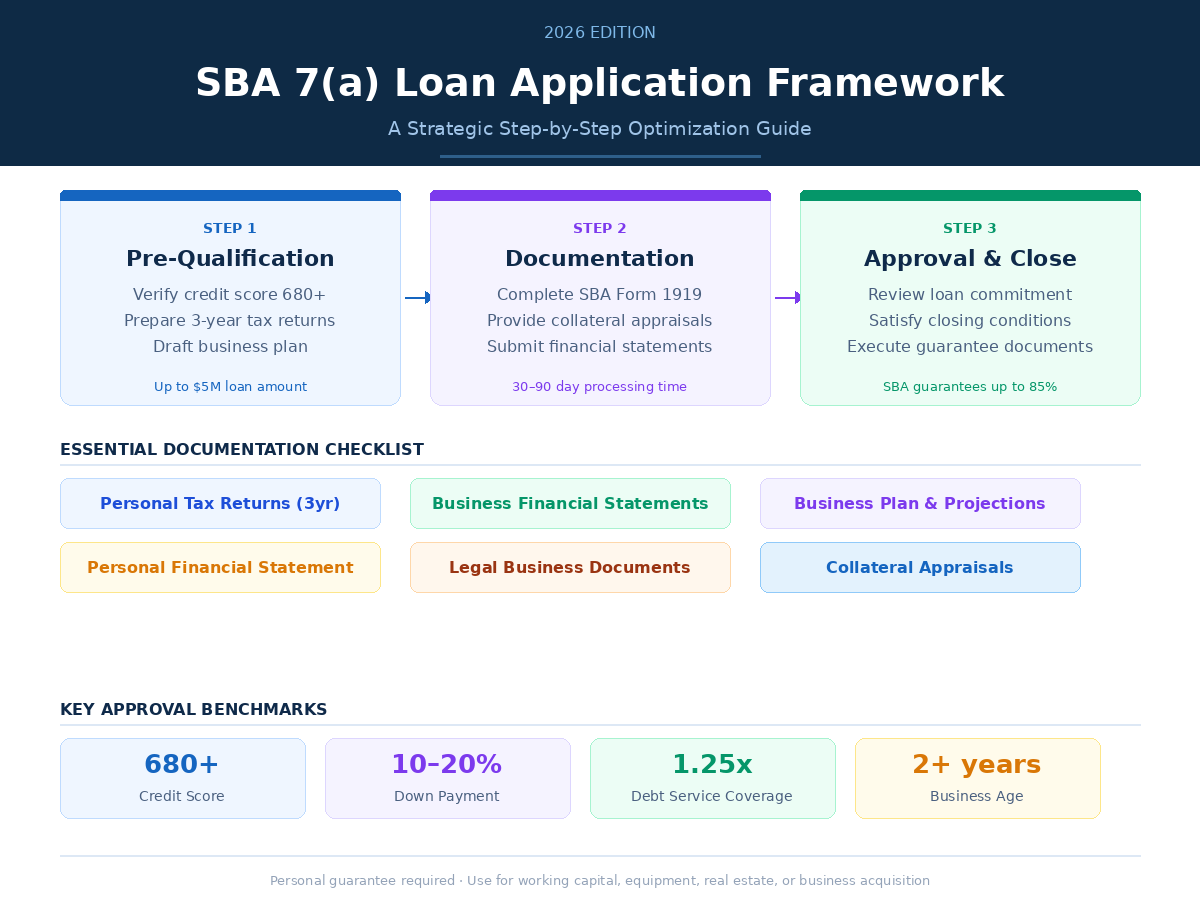

The landscape of American small business financing has undergone a seismic shift as we move through the second quarter of 2026. For entrepreneurs and established business owners alike, the SBA 7(a) loan remains the gold standard for flexible, government-backed capital, but the “how” and “when” of the application process have been fundamentally redefined by recent policy updates. Navigating this new framework requires more than just a solid business plan; it demands a strategic understanding of the latest regulatory pivots, from historic limit increases to tightened eligibility standards that took effect earlier this spring.

As of May 21, 2026, the most significant headline for growth-minded enterprises is the Small Business Administration’s recent announcement regarding cumulative lending caps. Effective July 4, 2026, the agency is doubling the combined limit for 7(a) and 504 loans to a record $10 million. By decoupling these two programs, the SBA now allows qualified borrowers to access up to $5 million through the 7(a) program for working capital and an additional $5 million through the 504 program for fixed assets. This change is a game-changer for capital-intensive industries like logistics and construction, providing a level of liquidity that was previously out of reach for many mid-sized small businesses.

However, with expanded access comes a more rigorous and localized underwriting environment. On March 1, 2026, the SBA officially sunset the use of the FICO Small Business Scoring Service (SBSS) for loans under $350,000. In its place, the agency has empowered individual lenders to use their own internal credit models, provided they adhere to a strict debt-service coverage ratio (DSCR) of at least 1.10:1. For the applicant, this means that “lender fit” is now more important than ever. Because your approval is no longer tied to a centralized government score, you must optimize your application to meet the specific risk appetite of your chosen bank or credit union. Success in this environment starts with a meticulous review of your historical and projected cash flow to ensure you comfortably exceed that 1.10 threshold.

Simultaneously, the SBA has tightened its stance on ownership. A critical policy update that went into effect this March now requires 100% of a business’s direct and indirect owners to be U.S. citizens or nationals residing within the United States. This rescinds previous exceptions that allowed for minority foreign ownership, making it imperative for companies with complex international equity structures to audit their cap tables before initiating the 7(a) process. This “America First” approach to lending is mirrored in the current fee structures for the 2026 fiscal year, which offer unprecedented advantages to the manufacturing sector. If your business falls under NAICS codes 31-33, you can currently benefit from a 0% upfront guaranty fee on 7(a) loans up to $950,000—a move designed to support the ongoing reshoring of American industrial production.

Interest rates in May 2026 have stabilized following the Federal Reserve’s late-2025 easing cycle, with the Wall Street Journal Prime Rate currently sitting at 6.75%. For a standard 7(a) loan over $250,000, variable rates are generally capped at Prime plus 2.25%, landing most well-qualified borrowers in the 9% APR range. While these rates are higher than the historic lows of the previous decade, the SBA’s expanded “use of proceeds” rules offer new ways to deploy this capital. In a nod to the technological revolution, the SBA now explicitly allows 7(a) funds to be used for AI-related expenses and digital infrastructure upgrades, recognizing these as essential tools for modern competitiveness.

To optimize your application within this 2026 framework, your first step should be a “pre-flight” eligibility check that goes beyond basic credit. Ensure your ownership structure is fully compliant with the new 100% citizenship rule and that your financial statements are prepared to withstand a lender-specific DSCR analysis. If you are a manufacturer, leverage the new Manufacturers’ Access to Revolving Credit (MARC) program or the 7(a) Working Capital Pilot (WCP) to minimize fees and maximize flexibility. By aligning your request with these specific 2026 priorities—high-tech integration, domestic ownership, and industrial growth—you position your business not just to secure a loan, but to thrive in an increasingly sophisticated economic environment. The window for these record-high limits and targeted fee waivers is open, but the winners will be those who approach the framework with a data-driven, strategic mindset.