As we navigate the midpoint of 2026, the American financial landscape has shifted into a complex new gear. For years, the high-yield savings account was the undisputed sanctuary for short-term capital, but the economic realities of today—May 21, 2026—demand a more sophisticated approach. With the Federal Reserve holding the benchmark interest rate in the 3.50% to 3.75% range and headline inflation recently ticking up to 3.8% due to persistent energy shocks, the “real” return on traditional cash is effectively zero or even slightly negative. To protect purchasing power and optimize liquidity, investors must look beyond the simple passbook and toward a strategic framework that accounts for the unique tax and regulatory environment of 2026.

The most significant shift this year stems from the implementation of the One Big Beautiful Bill Act, which took full effect on January 1st. By making the 2017 tax brackets permanent and significantly increasing the State and Local Tax (SALT) deduction limit to $40,400 for 2026, the federal government has fundamentally altered the math for tax-equivalent yields. For high earners in states like New York or California, the increased SALT cap makes municipal money market funds and short-term “munis” far more attractive than they were just twelve months ago. When you factor in the current hawkish tilt of the Federal Open Market Committee under the new leadership of Kevin Warsh, the potential for further rate hikes to combat war-induced inflation means that staying “short” on the yield curve is not just a safety play—it is a tactical necessity.

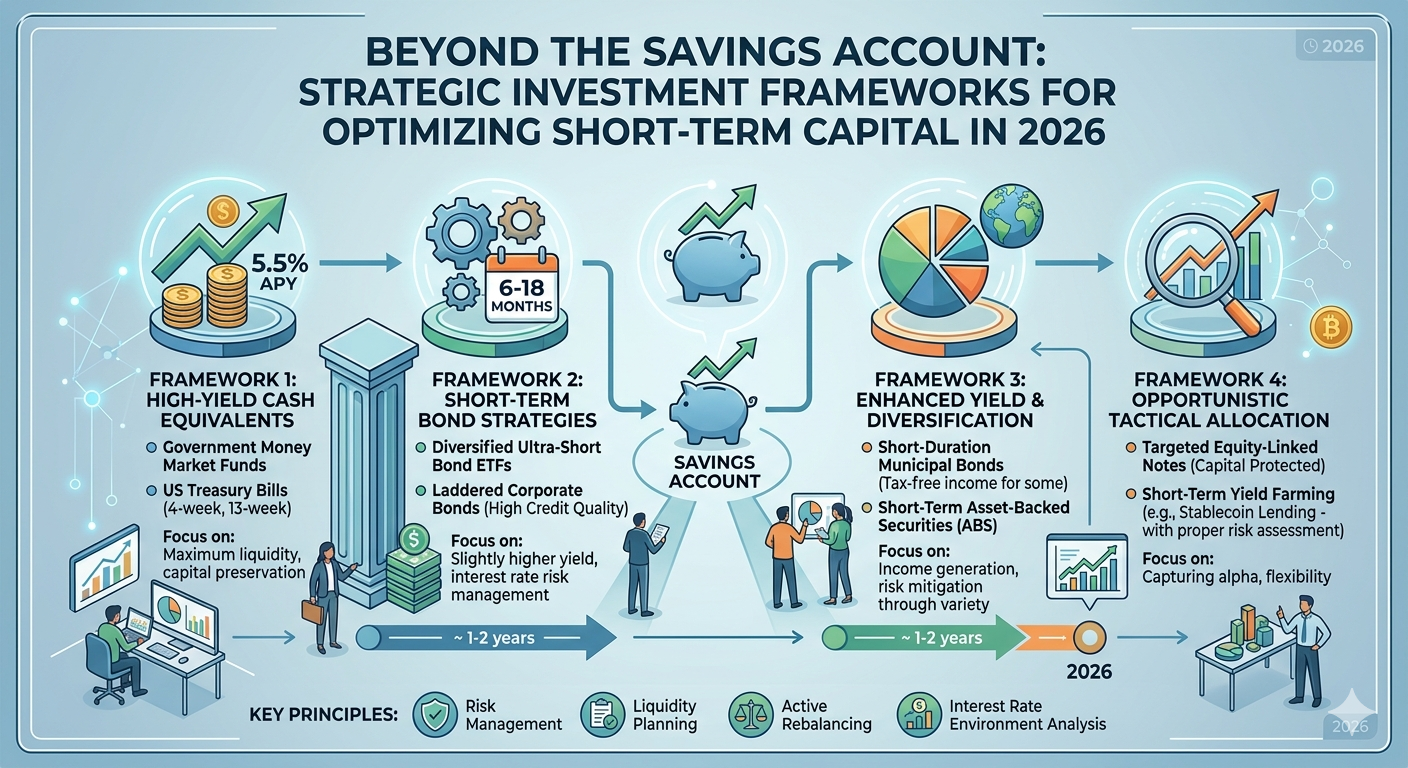

A modern framework for 2026 begins with tiered liquidity, a strategy that moves away from a single “emergency fund” bucket. Instead, savvy investors are bifurcating their short-term capital into “immediate” and “strategic” tiers. The immediate tier remains in high-yield accounts for instant access, but the strategic tier is increasingly flowing into the newly regulated world of tokenized money market funds. Following the SEC’s landmark 2025 rulings and the April 2026 implementation of intraday settlement for tokenized assets, these funds now offer something traditional mutual funds cannot: real-time liquidity without the T+1 settlement delay. By utilizing blockchain-based ledgers, these funds allow you to move from a yield-bearing asset into spendable cash in seconds, effectively eliminating the “cash drag” that used to plague brokerage accounts.

For those looking to park capital for three to six months, U.S. Treasury bills remain the gold standard, currently yielding around 3.6% to 3.7%. However, the 2026 strategy involves more than just buying and holding. With the 10-year yield recently touching 4.5%, the yield curve remains a focal point of volatility. Investors are increasingly using “laddered” T-bill strategies to ensure that a portion of their capital is always maturing and ready to be reinvested at potentially higher rates if the Fed decides to tighten further this summer. This laddering approach provides a natural hedge against the “inflation spike” we’ve seen in the wake of recent global energy disruptions, ensuring that your capital isn’t locked into yesterday’s lower rates while today’s prices at the pump continue to climb.

Furthermore, the 2026 tax landscape has introduced specialized vehicles that shouldn’t be ignored. The “Trump Accounts” for minors, which became available earlier this year, allow for up to $5,000 in annual after-tax contributions with tax-free growth—a powerful tool for parents looking to optimize short-term family capital. Similarly, the expanded flexibility of 529 plans, which now allow for higher K-12 withdrawal limits and broader applications for trade certifications, means that “short-term” education funds can be managed with much higher efficiency. By aligning these specific accounts with a portfolio of short-term corporate bond ETFs—which are currently offering a premium over Treasuries—investors can capture a 4% to 4.5% yield while maintaining the flexibility required for upcoming tuition or life expenses.

Ultimately, optimizing short-term capital in 2026 is about agility and tax intelligence. The days of “set it and forget it” in a standard savings account are over. Whether you are leveraging the new SALT deduction limits to favor municipal debt or utilizing tokenized funds for instantaneous liquidity, the goal remains the same: outpacing a stubborn 3.8% inflation rate while keeping your powder dry for future opportunities. As the Federal Reserve prepares for its June meeting amid a divided board, the most successful investors will be those who treat their cash not as a static reserve, but as a dynamic, strategic asset class. In this environment, the framework of tiered liquidity, tax-aware allocation, and technological integration is the only way to ensure your capital works as hard as you do.

Leave a Reply