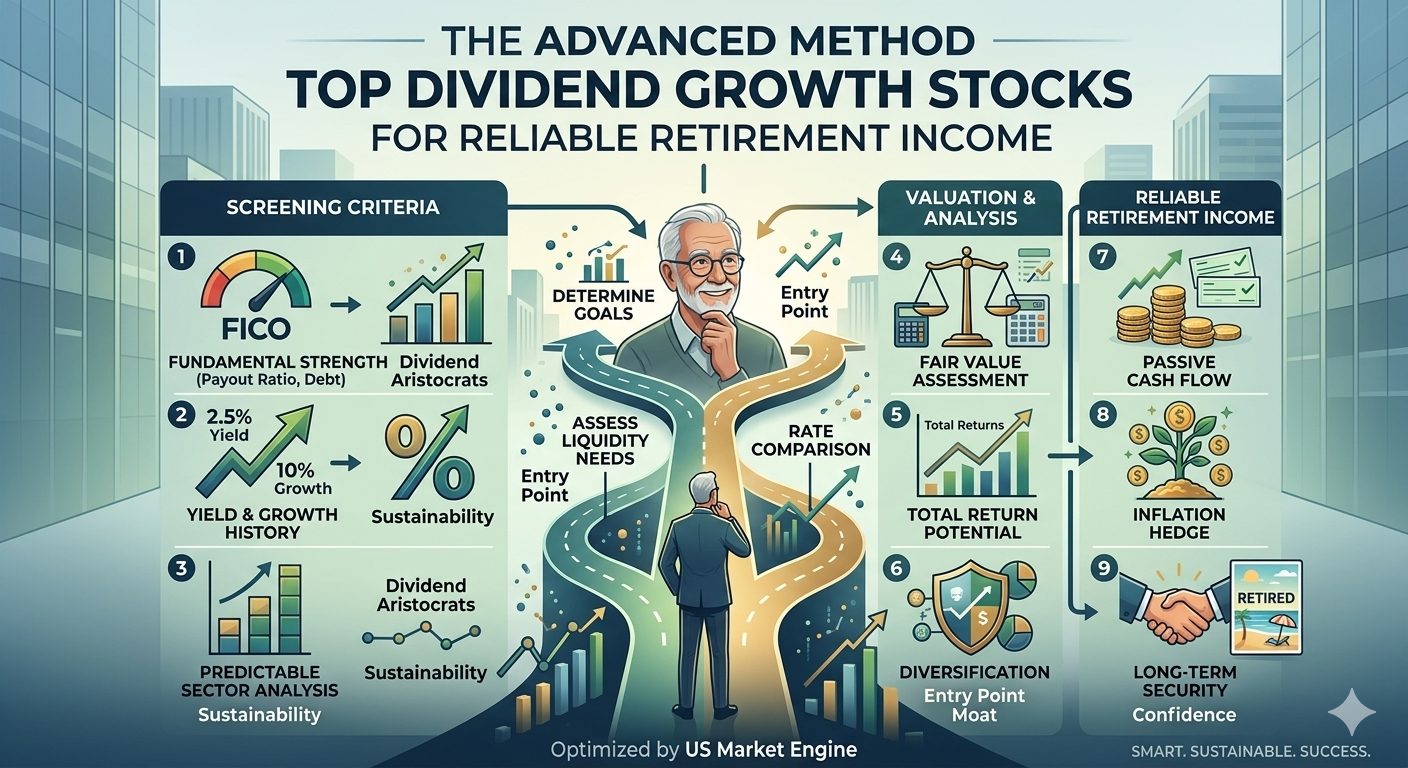

In the current economic landscape of May 2026, securing a reliable retirement income requires more than just a traditional “buy and hold” strategy. With the Federal Reserve maintaining interest rates in the 3.5% to 3.75% range and headline inflation hovering around 3.8% due to persistent energy pressures, the “Advanced Method” for dividend investing has shifted. It is no longer enough to simply chase the highest yields; instead, sophisticated investors are prioritizing dividend growth—the ability of a company to consistently increase its payout faster than the rate of inflation. This approach ensures that your purchasing power remains intact even as the cost of living climbs, a critical factor given the recent volatility in global energy markets and the ongoing economic shifts driven by the artificial intelligence boom.

The foundation of this advanced method lies in identifying “Dividend Aristocrats” and “Kings” that possess the free cash flow to sustain raises regardless of the macro environment. For instance, companies like Sysco (SYY), which recently celebrated 56 years of consecutive dividend increases, and Watsco (WSO), a leader in the HVAC sector with a 3.1% yield and a double-digit five-year growth rate, represent the type of resilience needed today. While high-yield options like Pfizer (PFE) offer an attractive 6.6% entry point, the advanced investor looks deeper at the payout ratio and earnings growth expectations for 2026 to ensure the dividend isn’t just a “yield trap” but a growing stream of wealth.

Tax efficiency is the second pillar of a successful 2026 retirement strategy. As of today, the IRS has adjusted contribution limits to account for the current inflationary environment, allowing individuals to shield more of their income from the taxman. For the 2026 tax year, the 401(k) contribution limit has risen to $24,500, while the IRA limit stands at $7,500. For those nearing retirement, the “super catch-up” provision introduced by SECURE 2.0 is now in full effect; if you are between the ages of 60 and 63, you can contribute an additional $11,250 to your workplace plan, bringing your total potential deferral to $35,750. However, a critical new policy for 2026 requires high earners—those with prior-year wages exceeding $150,000—to make these catch-up contributions on a Roth basis. This means paying taxes now to enjoy tax-free withdrawals later, a move that can be highly advantageous if you expect tax rates to rise in the future.

When managing these stocks in a taxable brokerage account, understanding the 2026 qualified dividend tax brackets is essential for maximizing your take-home pay. Most retirees will find their qualified dividends taxed at a preferential 15% rate, but for those with a total taxable income below $49,450 (single) or $98,900 (married filing jointly), that rate drops to a staggering 0%. Strategically timing your capital gains and dividend distributions to stay within these thresholds can effectively give you a “tax-free” raise. Conversely, high-net-worth investors must remain mindful of the 3.8% Net Investment Income Tax, which applies to those with modified adjusted gross incomes over $200,000 for individuals or $250,000 for couples.

Beyond the numbers, the advanced method requires a sector-specific lens tailored to the 2026 reality. Real Estate Investment Trusts (REITs) like Realty Income (O) remain a staple for their monthly distributions, currently yielding over 5%, which aligns perfectly with the monthly billing cycles of most retirees. Meanwhile, technology-adjacent dividend payers are gaining favor as the AI-driven productivity wave begins to reflect in corporate balance sheets. By focusing on companies with low debt-to-equity ratios and robust competitive moats, you protect your principal from the “hawkish drift” seen in recent Federal Reserve minutes.

Ultimately, the goal of top-tier dividend growth investing is to create a self-sustaining “income engine.” By reinvesting dividends during your final working years and then switching to cash distributions upon retirement, you leverage the power of compounding without the need to sell shares during market downturns. In a world where Social Security’s long-term outlook remains a topic of debate and traditional bond yields struggle to outpace core PCE inflation, this advanced method provides the autonomy and reliability necessary for a dignified American retirement. By staying informed on the latest IRS limits and focusing on quality over quantity, you can transform a volatile market into a source of enduring financial peace.

Leave a Reply