In the current financial climate of May 2026, many American homeowners feel caught in a high-interest pincer movement. With the Federal Reserve recently holding the benchmark rate steady at 3.50% to 3.75% and 30-year fixed mortgage rates hovering stubbornly around 6.82%, the dream of a sub-3% refinance feels like a relic of a distant past. However, the advanced method for securing a lower interest rate on an existing mortgage does not rely on waiting for a market-wide collapse in rates. Instead, it involves a sophisticated blend of psychological leverage, credit tier optimization, and the strategic use of lender retention protocols that most consumers never see.

To begin this advanced negotiation, you must understand the internal pressures facing US lenders today. In a market where purchase applications have slumped due to persistent inflation and Middle East-driven energy shocks, banks are terrified of losing the “good” loans they already have. This is your primary leverage. The process starts not with a customer service representative, but with a formal request to the lender’s retention or “loss mitigation” department. You are not asking for a favor; you are presenting a case for why it is more profitable for them to lower your rate than to lose your servicing rights to a competitor.

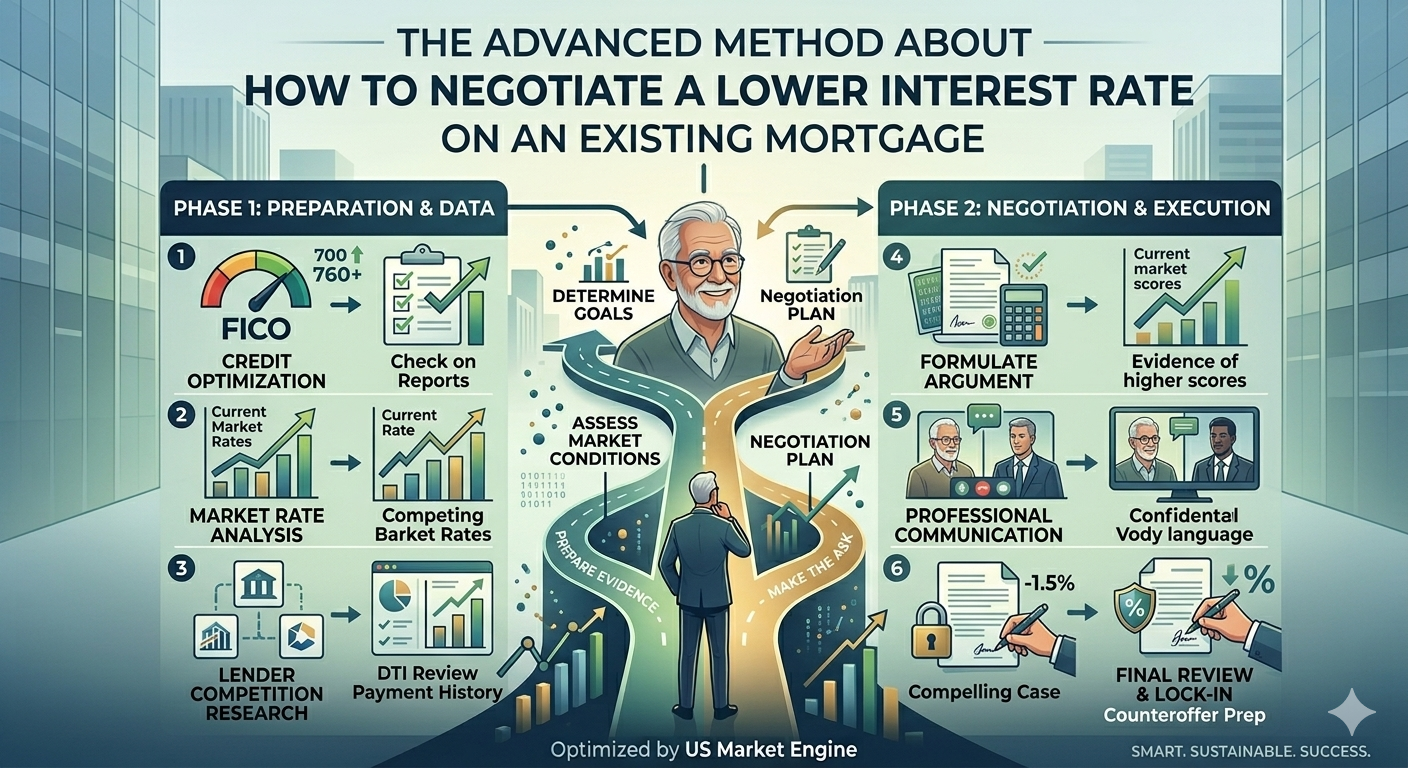

Before making that call, you must perform a “credit tier jump.” In 2026, the pricing gap between a 740 FICO score and a 780+ score has widened significantly. Lenders are currently rewarding “Financial Fort Knox” profiles with relationship discounts that aren’t advertised on their websites. If you have spent the last year paying down revolving debt or correcting errors on your report, you must present your updated profile as a reason for a “loan modification for credit improvement.” While traditionally used for hardship, savvy borrowers are now using this as a tool to request a rate adjustment based on their decreased risk profile.

Another advanced tactic involves the “Competing Quote Gambit” paired with a soft-pull credit authorization. Obtain a formal Loan Estimate from a digital-first lender or a local credit union, which are currently aggressive in their 2026 growth targets. Take this estimate to your current servicer’s retention officer and explicitly state that you are prepared to initiate a payoff. Because the cost for a lender to acquire a new customer in today’s market is estimated to be upwards of $3,000, they often have a “discretionary rate desk” that can shave 0.25% to 0.50% off your current rate just to keep the loan on their books. This is often referred to as a “rapid repricing” and avoids the thousands of dollars in closing costs associated with a traditional refinance.

If a direct rate cut is rebuffed, shift the negotiation to a “mortgage recast.” This is a powerful, underutilized tool in the 2026 toolkit. By making a lump-sum payment toward your principal—perhaps from a bonus or the sale of other assets—and paying a small administrative fee (usually around $250 to $500), the lender will re-amortize your loan based on the new, lower balance. While this doesn’t change the interest percentage itself, it dramatically lowers your monthly interest obligation and total interest paid over the life of the loan. In an era of 6.5% to 7% rates, the “effective” interest savings of a recast can often outperform the stock market’s current volatility.

Furthermore, do not overlook the impact of Private Mortgage Insurance (PMI). With home prices in many US markets having risen by 3.2% over the last year, you may have crossed the 20% equity threshold sooner than expected. Negotiating the immediate removal of PMI is equivalent to a significant “effective” rate reduction. An advanced move is to pay for a new appraisal to prove your loan-to-value ratio has dropped, then use that new valuation to demand a “tier-based rate review.”

Finally, persistence is the hallmark of the advanced negotiator. The mortgage market of May 2026 is defined by “two-speed” volatility; what a lender says “no” to on a Tuesday might be a “yes” on a Friday after a disappointing jobs report or a shift in 10-year Treasury yields. By positioning yourself as an informed, high-value borrower who understands the lender’s own cost of customer acquisition, you move from a position of asking for a break to one of negotiating a business deal. In this high-stakes environment, the lower rate doesn’t go to the person who waits for the Fed—it goes to the person who knows how to trigger the bank’s internal “save” protocols.

Leave a Reply