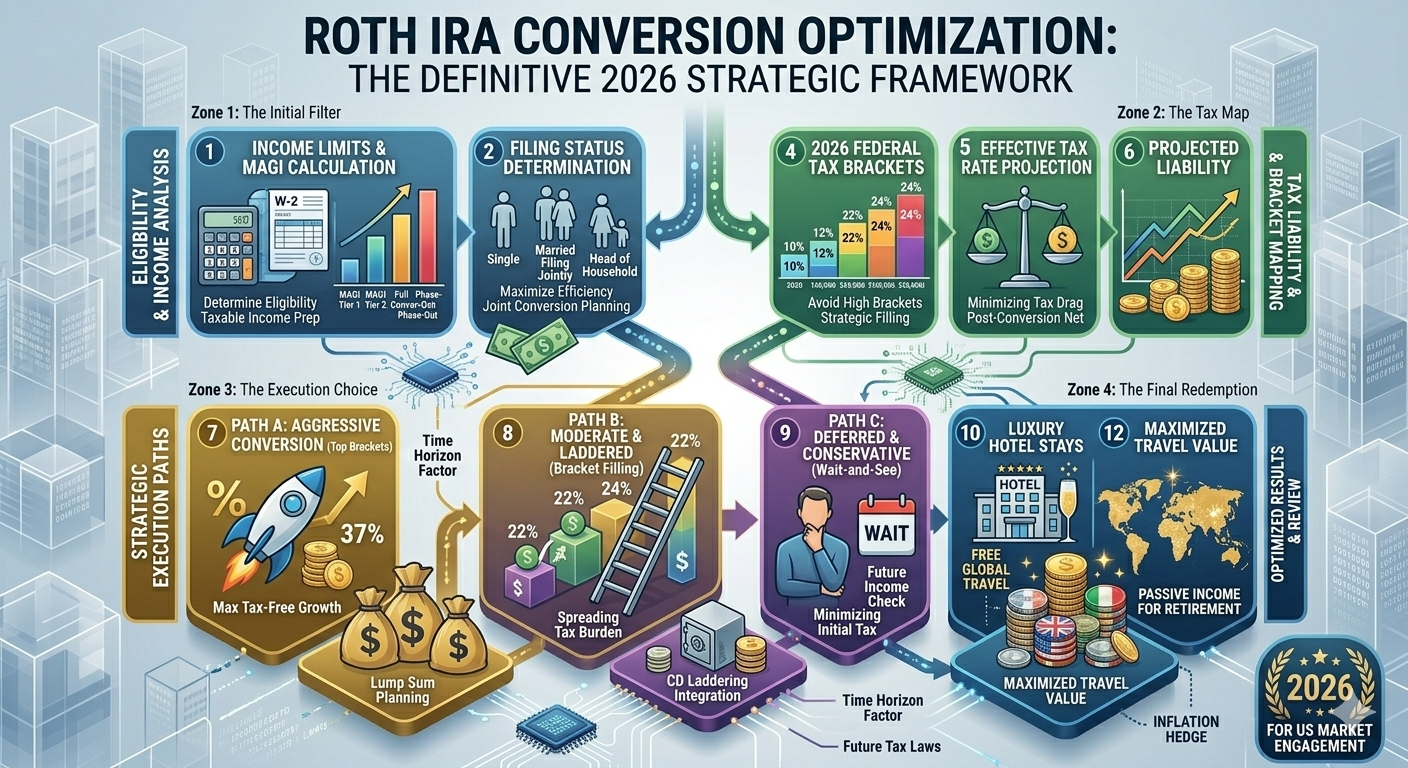

As we navigate the mid-point of 2026, the American retirement landscape has reached a pivotal juncture. With the recent passage of the One Big Beautiful Bill Act (OBBBA), which effectively made the 2017 tax reform brackets permanent, the “sunset anxiety” that dominated financial planning for years has finally dissipated. However, this new stability doesn’t mean you should settle for a passive strategy. In fact, the 2026 Strategic Framework for Roth IRA conversions is more nuanced than ever, requiring a sophisticated blend of tax bracket management, legislative compliance, and forward-looking asset allocation.

The foundation of any 2026 optimization plan begins with the updated Internal Revenue Service (IRS) limits. For the current tax year, the individual Roth IRA contribution limit has climbed to $7,500, with a catch-up provision for those aged 50 and older bringing the total to $8,600. For high-earning professionals, the income phase-out ranges have shifted upward to $153,000–$168,000 for single filers and $242,000–$252,000 for those married filing jointly. While these limits dictate direct contributions, the “Backdoor” and “Mega Backdoor” Roth strategies remain the primary engines for significant wealth migration into tax-free status, especially as the 24% tax bracket continues to offer a massive “sweet spot” for conversions, topping out at $403,550 for married couples.

One of the most significant shifts in the 2026 framework is the full integration of SECURE Act 2.0 provisions. We are now seeing the “Super Catch-up” in full effect for workers aged 60 to 63, who can contribute up to $11,250 to their workplace plans. Crucially, for those who earned more than $145,000 in the prior year, these catch-up contributions must now be made on a Roth basis. This mandate has fundamentally changed the “Traditional vs. Roth” debate for mid-career executives, effectively forcing a level of tax diversification that was previously optional. Furthermore, the 529-to-Roth rollover has become a mainstream tactical tool. In 2026, beneficiaries can move up to $7,500 of unused 529 funds into a Roth IRA, provided the account has been open for 15 years. This allows families to pivot educational savings into a retirement head-start without the sting of penalties.

Optimization in 2026 is not just about moving money; it is about the surgical precision of “bracket filling.” With the 24% marginal rate now a permanent fixture, the strategic goal for many retirees is to convert just enough traditional IRA assets to hit the ceiling of that bracket without spilling into the 32% tier. This is particularly vital for those in the “Golden Window”—the years between retirement and the start of Required Minimum Distributions (RMDs) at age 73 or 75. By aggressively converting during these low-income years, you effectively “pre-pay” your taxes at a known, lower rate, thereby shrinking the future RMDs that could otherwise trigger higher Medicare Part B and D premiums via the Income-Related Monthly Adjustment Amount (IRMAA). Remember that IRMAA uses a two-year lookback, so your conversion decisions today in May 2026 will

Leave a Reply